Ever heard the old saying, "A bird in the hand is worth two in the bush"? That's risk aversion in a nutshell.

It’s that natural human impulse to choose a guaranteed outcome over a riskier one, even when the risky option might lead to a bigger payoff. It's the reason most of us would take a sure $50 right now instead of a 50/50 coin flip for $100. This gut preference for certainty is a huge driver in how we all think about money, finance, and investing.

What Is Risk Aversion in Simple Terms?

At its heart, risk aversion isn’t about running from all risk. It’s about protecting what you’ve already got. You’re simply placing more weight on a known, even if smaller, reward than on an unknown one that could swing wildly between a huge gain and a painful loss.

This whole idea is a cornerstone of behavioral economics, the field that explores how our own psychology shapes our financial choices. The more formal concept behind it is called expected utility theory. It basically says that people make choices based on what brings them the most satisfaction, or "utility"—which isn't always the same as the highest potential dollar amount.

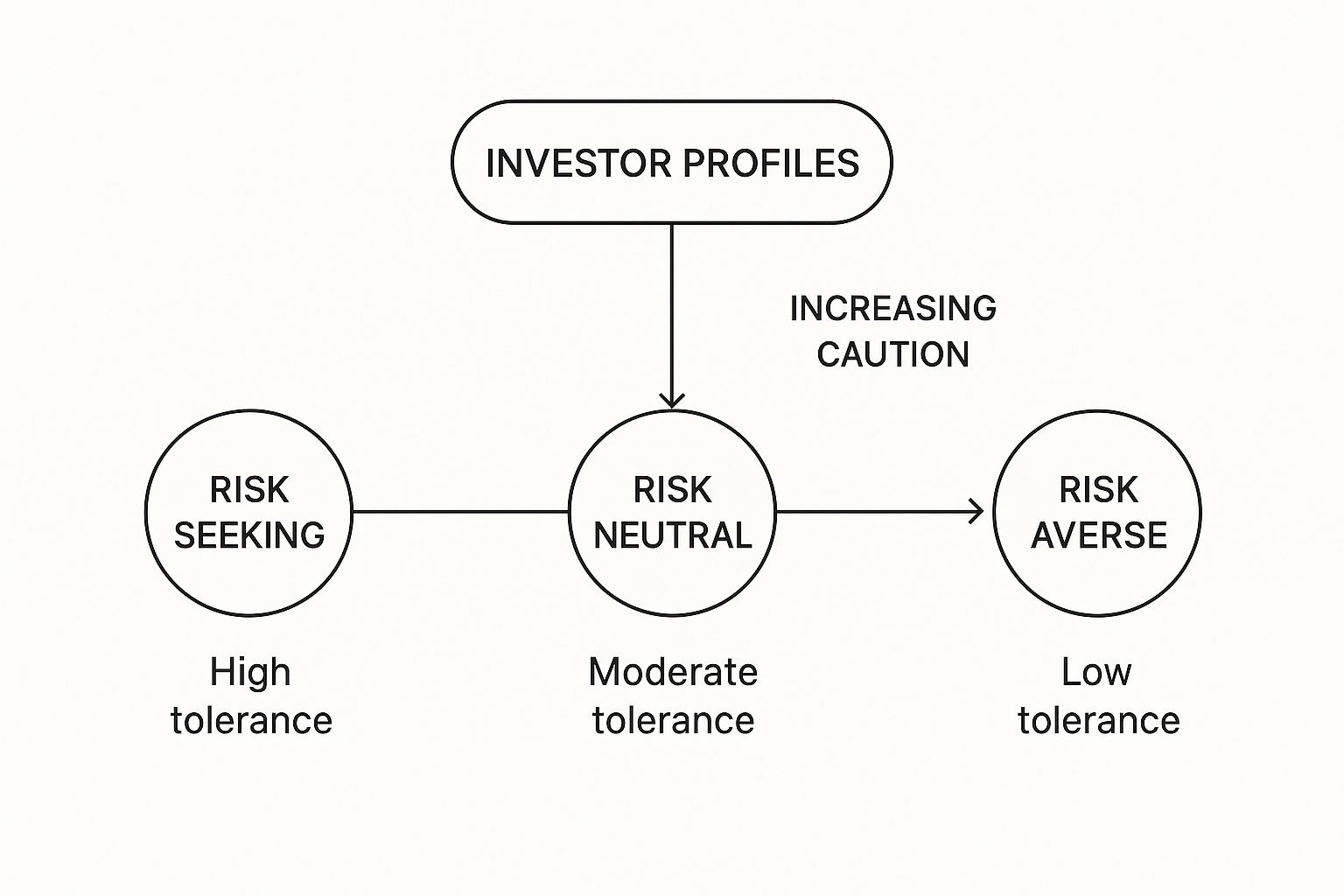

Understanding the Spectrum of Risk

Of course, not everyone has the same stomach for risk. Investors land all over a spectrum, from extremely cautious to boldly aggressive. Figuring out where someone falls on this spectrum helps put risk aversion into context.

- Risk-Averse: For these folks, the sting of losing money hurts way more than the joy of an equal gain. They put capital preservation first and are happy to accept lower returns for more safety. Think investments like bonds or stable, high-dividend stocks.

- Risk-Neutral: This type of investor is purely logical. They're indifferent between a sure thing and a gamble with the same expected value. The decision is all about the numbers, not the anxiety of uncertainty.

- Risk-Seeking: The complete opposite of risk-averse. These investors are drawn to the thrill of the gamble. They love high-volatility investments and are often willing to accept a lower expected return just for the shot at a massive home run.

This image gives you a simple visual of how these profiles stack up against one another.

As you can see, the risk-averse investor is at the most cautious end of the scale. It's a great reminder that risk tolerance isn't a simple "yes" or "no" switch—it's a continuum.

Investor Risk Profiles at a Glance

To make it even clearer, let's break down how these different investor types think and act. The table below compares the core behaviors and typical investment choices for each profile.

| Profile | Core Behavior | Typical Investment Choice |

|---|---|---|

| Risk-Averse | Prioritizes safety and is willing to accept lower returns to avoid losses. | Government bonds, blue-chip stocks, CDs. |

| Risk-Neutral | Focuses exclusively on expected returns, ignoring the level of risk. | Index funds, diversified portfolios that match the market. |

| Risk-Seeking | Is attracted to high-risk, high-reward scenarios, even with a chance of major loss. | Penny stocks, cryptocurrencies, venture capital. |

Ultimately, understanding these profiles isn't just academic. Knowing where you and other market participants fall on this spectrum is key to interpreting market sentiment and making smarter investment decisions.

The Psychology Behind Your Financial Decisions

To really get a handle on risk aversion, we have to look past the charts and portfolios and peer directly into the human mind. Ever wonder why a sudden 10% drop in your portfolio feels so much worse than a 10% gain feels good? The answer is a powerful cognitive bias known as loss aversion.

To really get a handle on risk aversion, we have to look past the charts and portfolios and peer directly into the human mind. Ever wonder why a sudden 10% drop in your portfolio feels so much worse than a 10% gain feels good? The answer is a powerful cognitive bias known as loss aversion.

This isn’t some abstract theory; it's a core part of how we’re wired. Psychologists have found that the pain of losing is roughly twice as powerful as the pleasure of an equivalent gain. Losing a $100 bill stings far more than the joy you feel from finding one. It’s not a sign of weakness—it’s just human nature.

This emotional quirk is a central piece of prospect theory, a game-changing concept in behavioral economics. It tells us our decisions aren't based on the final outcome, but on the potential for gains or losses from where we stand right now. We react to the same amount of money completely differently depending on whether we're about to gain it or lose it.

The Emotional Weight of a Loss

Let’s put this into a real-world context. Imagine your investment portfolio is sitting at $50,000. If it climbs to $55,000, you’ll feel pretty good. No doubt about it.

But what if it drops to $45,000? That $5,000 loss will likely unleash a much stronger emotional storm—fear, anxiety, and that gut-wrenching urge to sell everything just to make the pain stop.

That’s loss aversion in action. It’s the invisible hand that shoves investors into panic-selling at the very bottom of a market crash and makes them too nervous to buy when prices are low. Your brain is practically screaming, "Protect what you have!" while it only whispers, "Look at what you could gain."

Key Takeaway: Loss aversion creates an emotional imbalance in our financial choices. The fear of what we might lose often crushes the appeal of what we might gain, pushing us toward safer, more defensive moves.

How Cognitive Biases Steer Your Choices

Just understanding this psychological trigger is the first step toward making more rational decisions. The next time you feel that knot in your stomach during a market dip, you can recognize it for what it is: a natural, though not always helpful, cognitive bias. It’s not just about the numbers; it’s about the emotional stories we attach to them.

This emotional backdrop is what shapes the entire market mood. When millions of investors are gripped by loss aversion at the same time, it creates a tidal wave of fear. This collective emotion is exactly what sentiment indicators are designed to measure. To learn more, check out our guide on what social sentiment is and see how it reflects these shared feelings.

By recognizing your own tendencies toward risk aversion, you can learn to navigate these emotional currents without getting swept away.

How to Measure Your Own Risk Aversion

It’s one thing to understand risk aversion in theory, but how does it apply to you? Moving from an abstract idea to a practical self-check is the key to building a financial strategy that won’t keep you up at night. Fortunately, you don’t need complex formulas to figure it out—it really just starts with some honest self-reflection.

Financial advisors often use detailed risk tolerance questionnaires to get a handle on a client’s comfort level. These aren't simple "yes or no" quizzes. They present you with real-world scenarios to see how you weigh potential growth against the possibility of loss, giving you a much clearer picture of your financial DNA.

Key Questions to Ask Yourself

You can get a lot of the same insights just by thinking through the kinds of questions these professional questionnaires use. Be honest with yourself here. There are no right or wrong answers—only what’s true for you.

What's Your Timeline? How soon will you actually need this money? Someone saving for a house down payment in two years is going to see risk very differently than someone saving for retirement in 30 years. Shorter timelines usually demand more caution.

How Do You React to a Market Drop? Picture this: your portfolio loses 20% of its value in one month. What’s your gut reaction? Do you want to sell everything to stop the bleeding, or do you start thinking it might be a good time to buy? That emotional response is a huge clue.

What Do You Actually Know? How comfortable are you with different kinds of investments? An investor who has spent years studying the stock market will feel much less risk in stocks than someone who sticks to savings accounts and CDs.

A critical part of this is separating your emotional reaction from your financial capacity. You might feel panicked during a downturn (that's high risk aversion), but if your long-term goals are still perfectly on track, you have the financial ability to ride it out.

Your Past Behavior Is the Best Clue

Questionnaires are helpful, but your past actions tell the truest story. How you've behaved with your money during moments of stress or opportunity provides hard evidence of your natural tendencies. It’s about what you actually did, not just what you think you would do.

Taking a look at your financial history can be incredibly revealing. Ask yourself:

- Have you ever panic-sold? Think back to the last big market downturn. Did you sell investments at a loss because you were scared, only to watch the market recover without you? That's a classic sign of high risk aversion.

- Where do you keep your cash? Do you always have a big chunk of your money sitting in a low-yield savings or checking account, even when you have no plans for it? This preference for safety over growth points to a more cautious nature.

- What have you said "no" to? Think about investment opportunities you looked at but ultimately passed on. Was it because you felt they were too speculative or just too complicated? This pattern helps define the line you're unwilling to cross.

By digging into these real-world behaviors, you get past the hypotheticals. You get a raw, unfiltered look at your true comfort zone, and that's the foundation you need to build an investment strategy that actually fits who you are.

Risk Aversion in Your Investment Portfolio

Knowing you’re risk-averse is one thing, but translating that feeling into a real-world investment strategy is where it gets interesting. Your portfolio should be a direct reflection of how you feel about uncertainty. This is the moment you connect your own psychology to the assets you actually buy and hold.

For an investor who’s highly risk-averse, the number one goal is capital preservation. The fear of losing money is a much stronger motivator than the thrill of chasing high growth. Their portfolio is built like a fortress, designed for safety and stability, not spectacular gains.

This mindset naturally leads to certain investment choices. Forget chasing volatile tech stocks. Instead, the focus shifts to assets that crank out steady, predictable income and have a history of holding up well when the market gets rocky.

Building a Low-Risk Portfolio

If you’re a highly risk-averse person, your ideal portfolio probably feels solid and defensive. The core idea is to build something that minimizes those gut-wrenching downturns and lets you sleep at night.

A classic allocation for this kind of investor would heavily favor assets like:

- Government Bonds: Often considered one of the safest bets around. Bonds from stable governments pay out predictable interest and are far less volatile than stocks.

- Certificates of Deposit (CDs): These are essentially timed savings accounts offered by banks. You get a guaranteed return over a fixed period, and your initial investment is usually insured.

- Blue-Chip Dividend Stocks: Think shares in massive, established companies with a long track record of solid earnings and consistent dividend payments—like those in consumer staples or utilities.

A portfolio weighted 70-80% in fixed-income assets like bonds and CDs, with the remaining 20-30% in stable, dividend-paying stocks, is a common structure for someone prioritizing safety.

Constructing a Higher-Risk Portfolio

On the flip side, you have the risk-tolerant (or even risk-seeking) investor. They don't see market volatility as a threat; they see it as an opportunity for serious growth. They’re perfectly comfortable with the idea that to get higher potential rewards, you have to take on more significant risk.

Their portfolio will look completely different, built for capital appreciation rather than preservation. They are willing to stomach big swings in value for the chance at much bigger long-term gains.

You’ll often find these assets in a higher-risk portfolio:

- Growth Stocks: These are companies in fast-moving sectors like tech or biotech that plow their profits back into the business to fuel expansion instead of paying dividends.

- International and Emerging Markets: Investing overseas can unlock huge growth potential, but it also brings extra risks from currency swings and political instability.

- Alternative Investments: This broad category can include anything from real estate and private equity to cryptocurrencies. These assets often move independently of the stock market but come with their own unique set of risks.

Risk Aversion Beyond Your Portfolio

This whole idea of risk aversion goes way beyond just stocks and bonds. It quietly shapes major financial decisions all throughout your life. Just think about one of the biggest choices many people make: buying a home.

Deciding between a fixed-rate and a variable-rate mortgage is a perfect, real-world test of risk aversion.

A risk-averse person will almost always gravitate toward the certainty of a fixed-rate mortgage. Why? Because they know exactly what their payment will be for the next 15 or 30 years. It’s a shield against the risk of interest rates suddenly shooting up.

Someone more comfortable with risk might roll the dice on a variable-rate mortgage to snag a lower initial interest rate. They're essentially betting that rates will stay low or even drop. They trade long-term certainty for immediate savings, accepting the risk that their payments could jump in the future. That one choice says a lot about a person's preference for predictability over potential upside, showing just how deeply risk aversion is woven into our financial DNA.

Risk Aversion vs. Tolerance vs. Capacity

While "risk aversion" tells us how you feel about financial uncertainty, it’s just one piece of a three-part puzzle. Investors often get these concepts mixed up, confusing risk aversion with two other critical ideas: risk tolerance and risk capacity.

Getting this straight is crucial. Why? Because a mismatch between what you feel, what you're willing to do, and what you can actually afford is one of the quickest ways to make poor financial decisions.

Let's use an analogy. Imagine you're standing at the edge of the ocean.

- Risk Aversion is your gut reaction to the deep water—that instinctive fear of what lurks beneath.

- Risk Tolerance is how far from the shore you’re willing to swim to reach a cool-looking sandbar.

- Risk Capacity is your actual swimming skill and how long you can tread water if a strong current suddenly hits.

You need all three to line up to have a good (and safe) day at the beach. The same goes for investing.

What is Risk Aversion?

As we've touched on, risk aversion is all about emotion. It’s that knot in your stomach when the market takes a dive or the sense of relief you get from a guaranteed, safe return. It’s a psychological trait that dictates your comfort level with volatility and potential losses.

This is the collective "feeling" that sentiment tools like the Fear & Greed Index are designed to measure. For a deeper dive, check out our guide on understanding the Fear & Greed Index for trading.

Risk Aversion: Your emotional preference for a sure thing over a risky one, even if the risky option could pay off more. It’s all about how risk feels.

What is Risk Tolerance?

Risk tolerance is a step beyond pure feeling. It’s the amount of risk you are consciously willing to accept to hit your financial goals. It's a deliberate choice.

While your emotions (aversion) play a part, tolerance is more practical and tied to your objectives. For instance, you might be emotionally risk-averse but have a high tolerance for it because you're young and saving for retirement 30 years from now. You have time to recover from bumps in the road.

On the flip side, someone who loves the thrill of the market (low aversion) might have very low risk tolerance because they need their cash in six months for a down payment on a house.

What is Risk Capacity?

This is the most objective and arguably the most important of the three. Risk capacity has nothing to do with your feelings or your willingness—it’s about your cold, hard financial ability to absorb losses without wrecking your essential life goals.

Put simply, it's how much risk you can afford to take.

Factors like your income, savings, debts, dependents, and overall financial stability all determine your capacity. You might have a high tolerance for risk (you're willing to bet big!), but if you have a mountain of debt and no emergency fund, your capacity is actually very low.

Ignoring your capacity is like a non-swimmer agreeing to a deep-sea dive. The willingness might be there, but the ability isn't. It’s a recipe for disaster.

To help clear things up, here’s a simple table breaking down the three concepts.

Risk Aversion vs. Tolerance vs. Capacity

| Concept | What It Is | Example Question |

|---|---|---|

| Risk Aversion | Your emotional feeling about risk. | "How stressed would a 20% portfolio drop make you feel?" |

| Risk Tolerance | The amount of risk you are willing to accept. | "Are you willing to accept higher volatility for higher potential returns?" |

| Risk Capacity | The amount of risk you can afford to take. | "Could you still meet your essential financial goals after a major market loss?" |

Understanding the difference isn't just academic—it's fundamental to building a portfolio that lets you sleep at night while still working effectively toward your goals.

Gauging Market Fear with Sentiment Indicators

Risk aversion isn't just a personal quirk; it's a powerful force that can ripple across the entire market. When millions of traders and investors all feel that same gut-punch of loss aversion at once, it creates a collective mood. That mood is what we call market sentiment, and it usually swings between two extremes: fear and greed.

But how do you actually measure something as intangible as a "mood"?

That's where market sentiment indicators come in. Think of them as the market's thermometer. They analyze different data points that reflect what investors are doing—not just what they're saying—to give us a clear, simple reading of the market's psychological state.

The Fear and Greed Index

One of the most popular tools for this is the Fear & Greed Index. It takes a complex mix of seven different market signals and boils them all down into a single, easy-to-understand score ranging from 0 (Extreme Fear) to 100 (Extreme Greed).

What's it actually measuring? A few key things:

- Market Volatility: A big piece of the puzzle is the VIX, often nicknamed the "fear index." When the VIX spikes, it means uncertainty and fear are on the rise.

- Safe Haven Demand: This looks at how stocks are performing compared to safer bets like Treasury bonds. When money floods out of stocks and into bonds, you know investors are running for cover.

- Junk Bond Demand: This measures the gap in returns between stable, investment-grade bonds and riskier "junk" bonds. When that gap widens, it means investors are demanding a much higher reward for taking on risk—a clear sign of growing fear.

Here’s a snapshot of what the index looks like. It gives you a quick visual of where the market's head is at.

As you can see, the needle tells the story. It gives you an at-a-glance feel for whether the market is paralyzed by risk aversion or caught up in a frenzy of aggressive buying.

Key Insight: When the index is pointing to 'Extreme Fear,' it’s a sign of maximum risk aversion. This often means assets are getting oversold and could be undervalued. On the flip side, 'Extreme Greed' suggests investors have thrown caution to the wind, which is a classic warning sign of a potential market top.

Getting a handle on these signals helps you see the psychological undercurrents that are really driving prices. To dig deeper into putting these insights to work, check out our guide on how to use market sentiment analysis for trading. Once you learn to read these indicators, you’re not just understanding your own risk tolerance—you’re reading the mind of the market.

Common Questions About Risk Aversion

Even with a solid grasp of what risk aversion is, you probably have some practical questions about how it applies to your own financial life. Let's tackle a couple of the most common ones.

Can My Risk Aversion Change Over Time?

Absolutely. Your comfort with risk isn’t set in stone. Think of it as something that evolves right along with your life.

A young professional with a 30-year runway until retirement might feel perfectly fine loading up on riskier growth stocks. Fast forward a few decades, and that same person will likely feel very different as they near retirement. Their focus naturally shifts from aggressive growth to protecting what they’ve built.

Big life events are major catalysts, too. Getting married, having kids, or even receiving an unexpected inheritance can completely change your perspective on how much risk you're willing to take.

Key Insight: Your risk aversion is dynamic, not static. It’s smart to check in with yourself periodically—especially after a major life change—to make sure your investment strategy still feels right for you.

Is Being Risk-Averse a Bad Thing for Investing?

Not at all. This is a huge misconception. Being risk-averse doesn't mean you're a fearful or "bad" investor. It just means you place a high value on protecting your capital.

In fact, a healthy dose of risk aversion can be your best defense against making classic investing mistakes. It can stop you from chasing a hyped-up asset at its absolute peak or panic-selling everything during a temporary market dip.

The most successful investors are the ones who use a strategy that fits their personality. By acknowledging and respecting your own risk aversion, you can build a portfolio you'll actually stick with through thick and thin, which is the real secret to long-term success.

Ready to stop guessing and start measuring market sentiment? Fear Greed Tracker provides real-time Fear & Greed scores for over 50,000 assets, helping you gauge the market’s mood and make smarter, data-driven decisions. Explore live sentiment scores on feargreedtracker.com and turn market psychology into your strategic advantage.

Article created using Outrank