When you hear the term asset management fees, it's really just the price you pay for professional expertise. Think of it as hiring a financial expert or a whole firm to manage your investment portfolio, doing the heavy lifting of research, strategy, and ongoing maintenance needed to grow and protect your money.

What Exactly Are Asset Management Fees

Here's an analogy: your investment portfolio is like a high-performance race car. Sure, you could try to build it, tune it, and drive it yourself. But doing it well requires an incredible amount of time, skill, and insider knowledge.

Instead, you can hire a professional pit crew—engineers, mechanics, and a seasoned driver—to handle everything for you. Asset management fees are simply what you pay that expert crew to get the job done right.

This isn't just about picking a few stocks and calling it a day. It’s a continuous, hands-on process that covers a lot of ground:

- Deep-Dive Research: Sifting through thousands of potential investments to find the hidden gems that align with your financial goals.

- Portfolio Construction: Carefully building a diversified portfolio that’s tailor-made for your specific risk tolerance and long-term objectives.

- Constant Monitoring: Keeping a close eye on market movements, economic shifts, and the performance of every single one of your holdings.

- Strategic Rebalancing: Making smart adjustments along the way to ensure your portfolio stays on track and doesn't drift from your original plan.

At its core, you're paying for a disciplined process and dedicated expertise to help you navigate the often-choppy waters of the financial markets.

The True Cost of Professional Oversight

It's tempting to view these fees as just another line-item expense, but their real purpose is to deliver value that outweighs the cost. A great asset manager does more than just chase returns; they actively manage risk and, just as importantly, help you avoid the costly emotional mistakes that trip up so many individual investors, like panic-selling at the bottom of a market downturn.

The good news? Intense competition in the industry has been a huge win for investors, driving these costs down significantly. Over the past two decades, the average fee for mutual funds in the U.S. has been slashed by more than half, dropping from 0.86% to just 0.42% in recent years. Meanwhile, the average ETF fee is now a razor-thin 0.16%, a clear signal that lower costs are becoming the norm. For a deeper look, check out Morningstar's research on these fee trends.

Key Takeaway: Asset management fees aren't just arbitrary charges. They're payment for a whole suite of professional services designed to fine-tune your investment outcomes. The first step to making a smart decision is understanding exactly what you're paying for.

Now that we've covered the "why," let's get into the "what." While the overall cost landscape is looking friendlier, the fee structures themselves can vary quite a bit.

To help clear things up, here’s a quick breakdown of the most common types of fees you'll run into.

A Quick Look at Common Asset Management Fee Types

| Fee Type | What It Covers | Typical Structure |

|---|---|---|

| Management Fee | The core fee for professional oversight, research, and portfolio decisions. | A percentage of your total Assets Under Management (AUM), charged annually. |

| Performance Fee | An incentive-based fee paid only when the fund outperforms a specific benchmark. | A percentage of the profits generated above a predefined hurdle rate. |

| Expense Ratio | An all-in-one fee for mutual funds and ETFs covering operating costs. | An annual percentage of the fund's total assets, deducted automatically. |

Each of these fees serves a different purpose, and understanding how they work is key to figuring out the true cost of your investments.

Decoding the Different Types of Investment Fees

While the idea of asset management fees seems simple enough, the devil is always in the details. These fees aren't just one flat charge. Instead, they're a mix of different components, each paying for a specific part of the investment process. Learning to spot these distinct charges is like reading the nutrition label on your food—it shows you exactly what you’re getting.

The first and most common fee you'll run into is the management fee. This is the core payment for the professional expertise behind your portfolio. It pays the manager or firm for their research, analysis, and the critical buy-and-sell decisions they make for you. Think of it as the salary for your financial pilot.

For most investment accounts, this fee is a simple percentage of your total Assets Under Management (AUM), charged annually. If you have $100,000 managed at a 1% fee, you'll pay $1,000 for the year, often deducted from your account in smaller quarterly payments.

The Core Fee for Professional Management

The management fee is the bedrock of how most traditional investment advisors and many mutual funds get paid. Its main job is to cover the firm's operational costs, from salaries for portfolio managers and analysts to the research tools and tech they need to make smart decisions.

A manager's strategy often shapes this fee. An actively managed fund, where a manager is constantly researching and trading to beat the market, will almost always have a higher management fee than a passive index fund that just tracks a benchmark like the S&P 500.

The key thing to remember is that you're paying for a service. The goal is to make sure the value you get—through professional guidance, risk management, and potential returns—is worth the cost.

Performance Fees and Other Incentive Structures

Some investment vehicles, especially hedge funds and certain alternative investments, use a completely different approach called a performance fee. This is an incentive-based charge meant to align the manager's interests squarely with the investor's. Instead of just a flat rate, the manager only earns a bonus if they deliver returns above a specific target.

This often follows the famous "2 and 20" model. Here, the fund charges a 2% annual management fee on assets, plus a 20% performance fee on any profits that clear a certain benchmark or "hurdle rate." While this model rewards great performance, it's critical to understand the risks—it can encourage managers to take on more aggressive strategies. Choosing between a flat fee and a performance-based one often comes down to your financial goals and how you define risk aversion in your investor profile.

The All-in-One Expense Ratio

If you invest in mutual funds or Exchange-Traded Funds (ETFs), the most important number to watch is the expense ratio. This single percentage bundles nearly all of a fund's annual operating costs into one tidy figure.

Think of it as the "all-inclusive" price for a vacation—it covers a bundle of services, not just one. The expense ratio includes:

- Management Fees: The cost of paying the portfolio manager.

- Administrative Costs: Expenses for things like record-keeping, customer service, and sending out reports.

- 12b-1 Fees: Charges that cover the fund's marketing and distribution expenses.

- Other Operating Costs: Legal fees, accounting, and other day-to-day operational needs.

Because it's an all-in-one number, the expense ratio gives you a clear and simple way to compare the annual cost of different funds. A fund with a 0.50% expense ratio will cost you $5 a year for every $1,000 you invest. It’s a straightforward tool for any cost-conscious investor. By breaking down these fees, you go from being a passenger to an informed co-pilot on your financial journey.

How Asset Management Fees Are Calculated

Knowing the types of fees is one thing. Seeing how they actually get sliced out of your account is where it gets real. Let's get past the percentages and look at the simple math behind these costs.

Picture this: you have a $250,000 portfolio, and your advisor charges a straightforward 1% annual management fee. The math is easy enough.

$250,000 (Your Assets) x 0.01 (1% Fee) = $2,500

That $2,500 is your total annual fee. But you probably won't see it leave your account in one big chunk. Most firms bill quarterly to make the cost less of a shock. In this case, they’d just divide the annual fee by four, pulling $625 from your account each quarter.

Calculating Tiered Fee Structures

As your portfolio grows, you'll often start to benefit from a tiered fee structure. Think of it as a volume discount. The more you invest, the lower your percentage fee becomes. It’s the industry’s way of rewarding clients for trusting them with more capital.

Let's look at a hypothetical tiered schedule from an investment advisor:

- First $500,000: 1.00%

- Next $500,000 (up to $1M): 0.80%

- Next $1,000,000 (up to $2M): 0.60%

- Amounts over $2M: 0.40%

Now, say your portfolio is worth $1,200,000. The fee isn't a flat 0.60% on the entire amount. Instead, it works just like income tax brackets.

- The first $500,000 is charged at 1.00% = $5,000

- The next $500,000 is charged at 0.80% = $4,000

- The remaining $200,000 is charged at 0.60% = $1,200

Add it all up, and your total annual fee is $10,200 ($5,000 + $4,000 + $1,200). This blended rate is much better than a flat 1.00%, showing how a growing portfolio can lead to lower relative costs.

Demystifying the "2 and 20" Performance Fee

Things get a bit more complex with performance-based fees, especially the famous "2 and 20" model. You’ll find this structure with hedge funds and other alternative investments. It has two parts: a 2% management fee on all assets and a 20% performance fee on any profits.

Here’s how it plays out:

- Initial Investment: You put $1,000,000 into a hedge fund.

- Management Fee: The fund charges a 2% management fee, no matter what. That’s $20,000 for the year (

$1,000,000 x 0.02). - Performance: The fund manager has a fantastic year, and your investment grows to $1,300,000—a $300,000 profit.

- Performance Fee: The fund now takes 20% of that $300,000 profit, which comes out to $60,000 (

$300,000 x 0.20). - Total Fees: Your total bill for the year would be $80,000 (

$20,000management +$60,000performance).

The High-Water Mark: A critical protection for investors in this model is the high-water mark. This rule means the manager can only take a performance fee on new profits. If your portfolio value drops the next year, the manager has to get it back up to its previous peak before they can charge another performance fee. This keeps you from paying for the same gains twice.

Getting a handle on these calculations lets you read your statements with confidence, ask the right questions, and truly understand where your money is going.

The Hidden Impact of Fees on Your Investment Returns

It’s so easy to look at a 1% or 2% asset management fee and just write it off. A small price to pay for professional help, right? But that’s probably one of the most dangerous assumptions you can make as an investor. Over time, that tiny percentage doesn't just chip away at your returns—it actively compounds against you.

Think of it like a tiny, slow leak in a huge water tank. Day to day, you’d never notice the water level dropping. But give it a few years, and that steady drip, drip, drip could leave the tank half-empty. Fees do the exact same thing to your portfolio, quietly siphoning away your future wealth when you're not looking.

Let's make this real. Imagine two friends, Alex and Ben, each investing $100,000. Both of their portfolios manage to earn an average of 7% a year for the next 30 years. The only catch? Alex is in a low-cost fund with a 0.5% annual fee, while Ben chose an actively managed fund charging 1.5%.

The Long-Term Cost of a 1% Difference

That 1% difference feels almost meaningless at first. But watch what happens when you let the clock run for three decades. The gap starts small, but as the years go by, the chasm between their final account balances becomes staggering. It's a masterclass in how compounding can work for you—or against you.

To really see the damage, let's look at the numbers.

The 30-Year Impact of Fees on a $100,000 Investment

This table shows just how much that seemingly small fee difference can cost over an investing lifetime. We'll track Alex's and Ben's $100,000 initial investment, assuming a 7% annual return before fees.

| Annual Fee | Value After 10 Years | Value After 20 Years | Value After 30 Years |

|---|---|---|---|

| 0.5% (Alex) | $187,714 | $352,365 | $661,226 |

| 1.5% (Ben) | $170,814 | $291,776 | $498,388 |

| Difference | $16,900 | $60,589 | $162,838 |

After 30 years, Ben ends up with $162,838 less than Alex. That’s not a rounding error; it’s a life-changing amount of money. It’s the difference between retiring comfortably and having to work a few more years. It's an opportunity cost of massive proportions.

Here's the key takeaway: You can't control what the market does day-to-day. But you have 100% control over the fees you agree to pay. Minimizing costs is one of the surest ways to maximize what you end up with.

Why Fee Compression Matters to You

This laser focus on costs has kicked off a huge shift in the investment world. Even as the industry’s total Assets Under Management (AuM) ballooned from $84.9 trillion in 2016 to a recent estimate of $145.4 trillion, fee revenue hasn't kept pace. Why? Because investors are getting smarter and moving their money to cheaper funds, forcing firms to lower their prices to compete. You can get a deeper dive into this trend from these insights on global asset management.

This is fantastic news for you. It means finding low-cost, high-quality investments is easier than ever.

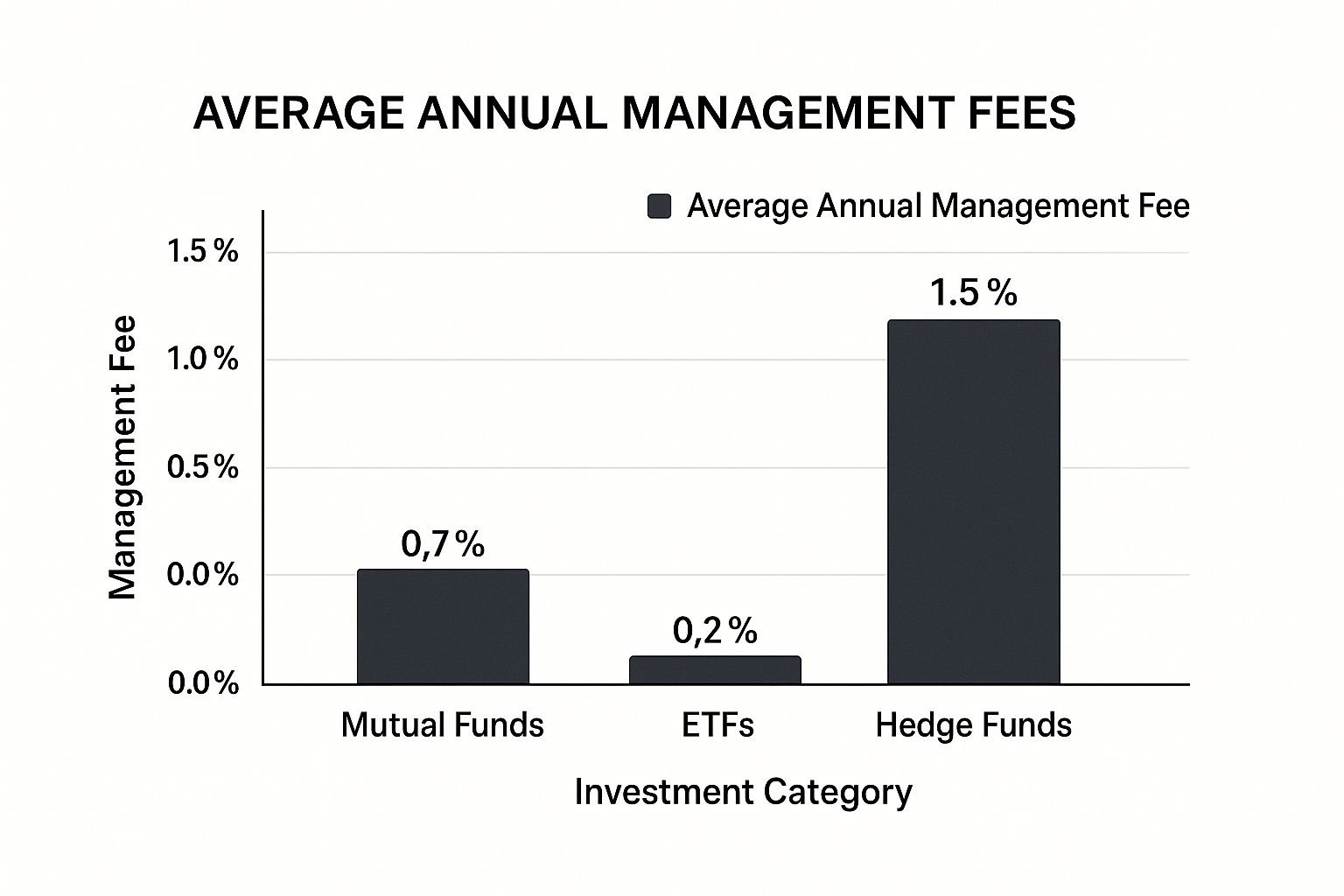

This chart drives the point home, showing the typical fees for different types of investments.

As you can see, ETFs are, on average, far cheaper than their mutual fund counterparts and a world away from the high costs of hedge funds. For anyone looking to keep more of their money, they’re an obvious place to start.

The moment you stop seeing fees as a small expense and start seeing them as a major roadblock to your long-term wealth, everything changes. It’s the lightbulb moment that can completely reshape your financial future.

Actionable Strategies to Lower Your Investment Costs

Knowing how much fees can eat into your returns is one thing. Actually doing something about it is what pads your retirement account. Think of high asset management fees as a constant drag on your portfolio's momentum. The good news? You have plenty of power to fight back and keep more of your money working for you.

The most straightforward move is to pick investment vehicles that don't cost an arm and a leg. When it comes to the classic showdown between active and passive management, there’s a clear winner on the cost front.

Actively managed funds—the ones with teams of analysts trying to outsmart the market—almost always carry higher price tags. On the flip side, passive index funds and Exchange-Traded Funds (ETFs) have a simpler job: just track a market index like the S&P 500. Less human meddling means significantly lower fees.

Choose Low-Cost Funds and ETFs

Building your portfolio around low-cost index funds and ETFs is probably the single biggest lever you can pull to boost your long-term results. This isn't about being cheap or sacrificing quality. It's about accepting a simple truth: over decades, cost is a far better predictor of your actual, take-home returns than any star manager's past winning streak.

Just look at the math. Choosing an S&P 500 ETF with a 0.03% expense ratio over an active fund charging 0.80% gives your portfolio an immediate, built-in advantage. That simple switch means more of the market's gains end up in your pocket, year after year.

This pressure isn't just on investors; asset managers feel it, too. The whole industry is grappling with fee compression while their own costs keep rising. In fact, total costs for these firms have been climbing at a compound annual rate of 6%, thanks to competition for talent and a shift to more complex products. Many are scrambling to get leaner just to stay in the game, as detailed in a report on the industry's push for resilience on BCG.com.

Explore Modern Alternatives and Negotiate

Technology has thrown open the doors to some great, low-cost alternatives to the old-school financial advisor. Robo-advisors, for instance, use algorithms to build and manage diversified portfolios for a fraction of the price, typically charging between 0.25% and 0.50% a year. They're a fantastic option if you want a hands-off, professionally managed portfolio without the hefty price tag.

And if you have a larger portfolio and work with a traditional advisor, don't just assume their fees are non-negotiable. For clients with significant assets, many advisors are willing to talk.

Pro Tip: Don't be shy about asking for a fee reduction. The worst they can do is say no. Do your homework first—benchmark their fees against competitors and remind them of the size of your account.

Finally, make a habit of being your own best advocate. That means doing more than just a quick glance at your account balance once in a while.

Your Fee-Reduction Checklist:

- Review Your Statements: When that quarterly or annual statement arrives, actually read it. Hunt for any line items that mention management fees, administrative costs, or other charges.

- Question Everything: See a fee you don’t recognize? Pick up the phone. Ask your advisor or the fund company for a plain-English explanation. What is it for? How is it calculated?

- Leverage Analyst Insights: Fees are only part of the puzzle. It's also vital to know if the investments you're paying for are any good. You can learn more about how to understand stock analyst ratings to make smarter calls on whether an investment is truly worth its cost.

By staying informed and proactive, you can systematically cut down the drag from fees and make sure your path to long-term wealth is as efficient as possible.

Your Top Questions About Investment Fees, Answered

Alright, we've covered the different types of fees, how they're calculated, and the serious dent they can make in your returns over time. But you probably still have some practical questions buzzing around. Let's tackle them head-on.

Think of this as the final, practical checklist to clear up any confusion and help you get a real handle on your investment costs.

How Do I Find Out What Fees I’m Actually Paying?

This part requires a little detective work, but the clues are all there if you know where to look. Your two best friends here are your account statements and the fund's prospectus.

- Your Account Statements: Grab your latest quarterly or annual statement from your brokerage or advisor. Scan it for line items like "management fee," "advisory fee," or "administrative fee." These are usually pulled right out of your account's cash balance.

- The Fund Prospectus: For any mutual fund or ETF, the expense ratio is the magic number. You'll find it in the fund’s summary or statutory prospectus, typically in a fee table right at the beginning of the document. This single percentage bundles together management, administrative, and other operational costs.

If you can't find these details or the language is confusing, don't just guess. Call your advisor or the fund company. Seriously. Asking, "Can you walk me through every single fee I'm paying?" is one of the most powerful moves you can make as an investor.

Nailing down your fees is a non-negotiable first step. It’s as fundamental to a solid investment strategy as understanding market psychology is to making smart trades. To learn more about how the market "thinks," check out our guide on how to use market sentiment analysis for trading.

What Is a Reasonable Fee to Pay?

The million-dollar question: "What's a fair price?" The honest answer is, it completely depends on what you're getting for your money. There’s no single "right" fee, but we can look at some clear industry benchmarks to see if you're in the right ballpark.

- Robo-Advisors: For a simple, automated portfolio, you should be paying somewhere between 0.25% and 0.50% a year. It's a great, low-cost way to get a professionally managed, diversified portfolio without needing a ton of complex financial planning.

- Traditional Financial Advisors: If you're getting the whole package—comprehensive financial planning, retirement strategy, tax help, and a custom-built portfolio—fees often start around 1.00% of your assets. This percentage usually drops as your portfolio gets bigger.

- Mutual Funds & ETFs: For a passive index fund that just mirrors the market (like an S&P 500 fund), anything over 0.20% should make you pause. For actively managed funds, where a manager is trying to beat the market, fees can run from 0.50% to over 1.00%. Here, you have to ask yourself: is that higher cost actually delivering consistently better performance?

It all comes down to value. A higher fee might be worth it if it includes detailed financial planning and tax strategies. But for basic investment management you could get cheaper elsewhere? Not so much.

Are My Investment Fees Tax Deductible?

This is a huge point of confusion for many people, especially since the rules changed recently. In the past, you could deduct certain investment expenses, including advisory fees, on your taxes.

However, the Tax Cuts and Jobs Act of 2017 got rid of that deduction for most of us. So, as it stands now, asset management fees you pay from a regular taxable brokerage account are generally not tax-deductible.

There is one small exception. When fees are taken directly from a tax-deferred retirement account, like an IRA or 401(k), they're paid with pre-tax dollars. This reduces the account's value but doesn't create a separate tax bill. It's a tiny silver lining, but the direct deduction on your tax return is gone. As always, it's best to talk to a tax professional for advice tailored to your specific situation.

At Fear Greed Tracker, we believe that understanding every aspect of investing—from fees to market sentiment—is crucial for success. Our tools provide real-time Fear & Greed scores for over 50,000 assets, empowering you to see the market's mood and make data-driven decisions. Transform fear into your strategic advantage and start building a smarter portfolio today at https://feargreedtracker.com.