You've probably heard the term Dollar Cost Averaging (or DCA) tossed around in investing circles. It sounds technical, but the idea is actually incredibly simple. At its core, DCA is an investing strategy where you commit to investing a fixed amount of money on a regular schedule, no matter what the market is doing.

This simple discipline means you end up buying more shares when prices are low and fewer shares when they're high. Think of it as putting your investing on autopilot to sidestep emotional decisions and reduce risk.

What Is Dollar Cost Averaging in Simple Terms?

Let's forget stocks for a second and think about your weekly grocery run. Imagine you love avocados and buy them every single week, spending exactly $5.

Some weeks, they’re a steal at $1 each, so your $5 gets you five avocados. Other weeks, a bad harvest spikes the price to $2.50, and that same $5 only gets you two. Without even thinking about it, you naturally bought more when they were cheap and fewer when they were expensive. Over time, you’d get a pretty decent average price per avocado without ever trying to time the "avocado market."

That's exactly how Dollar Cost Averaging works with your investments. It takes the guesswork out of the equation. Instead of trying to nail the absolute perfect moment to buy—a game even the pros rarely win—you just stick to a consistent, automatic plan.

To break it down even further, here's a quick look at the core components of the DCA strategy.

Dollar Cost Averaging At a Glance

| Component | Description |

|---|---|

| Fixed Investment Amount | You decide on a set amount of money to invest each period (e.g., $100, $500). |

| Regular Intervals | You choose a consistent schedule, like weekly, bi-weekly, or monthly. |

| Market Agnostic | The investment happens automatically, whether the market is up, down, or sideways. |

| Long-Term Focus | This strategy is designed for building wealth over time, not for short-term trading. |

This table shows just how straightforward the mechanics are. The real power is in its consistency.

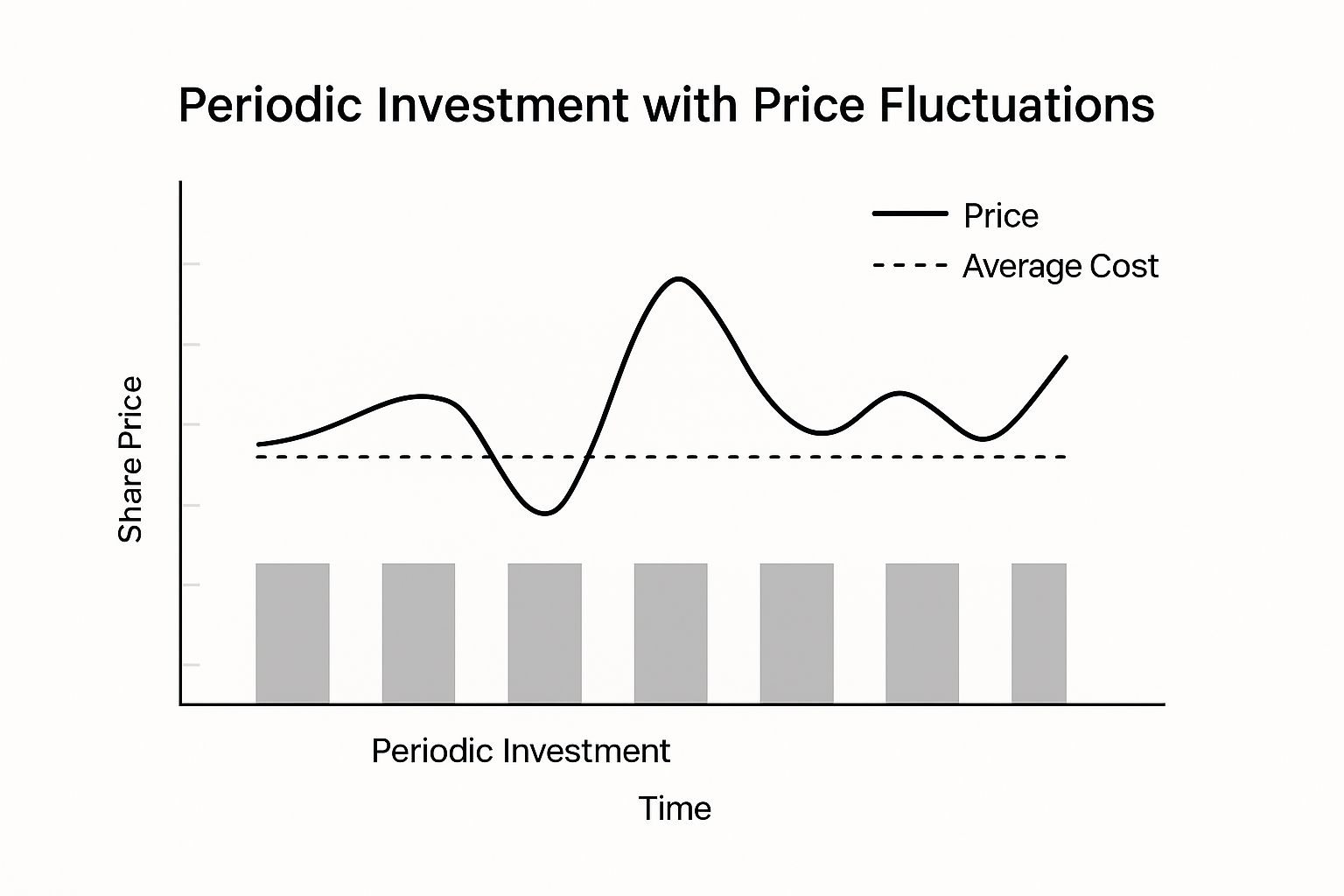

The Core Mechanics of DCA

The whole strategy is built on one thing: consistency. By investing the same dollar amount on a fixed schedule—say, $200 on the first of every month—you take emotions and overthinking completely out of the picture. This simple act has a surprisingly powerful effect over the long haul.

When the market takes a nosedive and prices drop, your $200 automatically buys you more shares than it did the month before. On the flip side, when the market is flying high, that same $200 buys you fewer shares.

This disciplined process naturally smooths out your average cost per share over time. It turns market volatility, which most investors fear, into a potential ally by making sure you're accumulating more assets when they're on sale.

So, what is dollar cost averaging at the end of the day? It’s a system. It’s a framework that forces you to buy low while preventing you from getting carried away and buying too much when prices are sky-high. This simple habit removes the anxiety of dumping a large sum of money into the market at the worst possible time and helps you build your wealth steadily and calmly.

How Dollar Cost Averaging Works in the Real World

Alright, let's move past the theory and see how dollar cost averaging plays out in a real-world scenario.

Meet Sarah, a new investor. She decides she wants to put some money into a popular index fund. Instead of trying to time the market, she commits to investing $100 every single month, no matter what the headlines are saying.

Her plan is simple: invest a total of $600 over six months. Let's see how this steady approach navigates the typical ups and downs of the market.

Sarah’s Six-Month Investment Journey

Sarah sets up an automatic transfer for the first of each month. Here’s a play-by-play of how her investment unfolds as the share price wobbles.

- Month 1: The fund's share price is $10. Her $100 investment nabs her 10 shares. A solid start.

- Month 2: The market takes a dip, and the price falls to $8. Bummer? Not for Sarah. Her $100 now buys 12.5 shares.

- Month 3: The price drops even further to $5. While others might be panicking, her $100 buys a whopping 20 shares this month.

- Month 4: The market shows signs of life, climbing back to $8. Her $100 gets her another 12.5 shares.

- Month 5: Optimism is back! The price jumps to $12. This time, her $100 buys 8.33 shares.

- Month 6: The price steadies at $11. Her final $100 investment adds 9.09 shares to her portfolio.

After six months, Sarah has invested her full $600. When you add up all the shares she bought each month, she now owns a total of 72.42 shares.

So, what was her average cost per share? We just divide her total investment by the number of shares she owns ($600 / 72.42 shares).

The math shows Sarah’s average cost per share works out to be just $8.28.

This is the magic of DCA in action. The chart below shows how her fixed monthly investment meant she automatically bought more shares when they were cheap, bringing her overall average cost down.

As you can see, Sarah’s average cost per share ($8.28) is actually lower than the average market price over that same six-month period ($9.00). That’s the strategy doing its job.

Comparing DCA to Lump Sum Investing

Now, let's bring in another investor, Mark. He had the same $600 to invest but decided to go all-in at once—a lump sum investment. He put the entire amount into the market in Month 1, when the share price was $10.

Mark’s $600 bought him exactly 60 shares ($600 / $10 per share). He then had to sit and watch as the price dropped in the following months.

So, how did they both end up? Let's break down the numbers side-by-side to see the real impact of their different approaches.

DCA vs Lump Sum: A Hypothetical Investment

| Month | DCA Investment | Stock Price | Shares Bought (DCA) | Lump-Sum Shares (Bought Month 1) |

|---|---|---|---|---|

| 1 | $100 | $10 | 10.00 | 60 |

| 2 | $100 | $8 | 12.50 | - |

| 3 | $100 | $5 | 20.00 | - |

| 4 | $100 | $8 | 12.50 | - |

| 5 | $100 | $12 | 8.33 | - |

| 6 | $100 | $11 | 9.09 | - |

| Total | $600 | - | 72.42 | 60 |

The table makes it clear: Sarah's steady, automated approach allowed her to accumulate more shares for the same amount of money.

By the end of the six months, when the share price landed at $11, Sarah's 72.42 shares were worth $796.62—a $196.62 gain. Meanwhile, Mark's 60 shares were worth $660, giving him a gain of just $60.

This simple comparison shows the true power of dollar cost averaging, especially in a shaky market. It takes the stress of "perfect timing" out of the equation. While Mark's investment was a victim of bad luck, Sarah’s disciplined strategy turned market dips into buying opportunities, leading to a much better outcome.

The Hidden Power of a Disciplined Mindset

Let's be honest: successful investing is less about staring at complex charts and more about keeping your own emotions in check. It’s a constant tug-of-war between two powerful forces: the fear of losing your hard-earned money and the greed that whispers, "Don't miss out!"

This is where dollar cost averaging really shines. It's a powerful tool because it directly tackles these psychological hurdles head-on.

By putting your investments on autopilot, you eliminate the single most paralyzing question every investor faces: “Is now the right time to buy?” That hesitation can leave you stuck on the sidelines for months, watching potential gains pass you by. A DCA plan makes the decision for you, turning investing into a consistent, unemotional habit.

This disciplined approach is your secret weapon for navigating the market’s inevitable ups and downs. It helps you resist the urge to panic-sell when prices drop or chase a hot stock at its peak. Instead of reacting to scary headlines, you just stick to the plan.

Turning Regret Into Opportunity

One of the biggest emotional traps in investing is regret. We've all felt it. Imagine putting a large chunk of cash into the market right before a major downturn. That feeling can be absolutely crushing, and it often leads to terrible decisions.

DCA completely flips that script.

With dollar cost averaging, a market downturn is no longer a source of regret; it's a built-in opportunity. Your next scheduled investment simply buys more shares at a lower price, reinforcing positive, disciplined behavior.

This framework acts as a psychological safety net, especially when the market gets choppy. It dials down the anxiety and encourages you to stay invested, which is where long-term returns are really made. Many seasoned investors use this strategy not just for financial reasons, but to keep their cool when things get wild. As a recent article on bernstein.com points out, it's about managing your emotional response to market swings.

Automating Discipline for Better Outcomes

The human brain is wired with biases that can wreck even the most brilliant investment strategies. These mental shortcuts often cause us to buy high out of excitement and sell low out of fear—the exact opposite of what we should do.

You can learn more about how these tendencies mess with your portfolio in our guide on what is behavioral finance and how does it work.

Setting up automatic transfers is like building a fortress of discipline against these impulses. It removes the daily temptation to second-guess your strategy based on market noise.

Over time, this steady, unemotional approach to building your portfolio almost always leads to better results than trying to perfectly time every single buy and sell. It's a simple, yet incredibly powerful, way to make sure your actions align with your long-term goals.

So you've got a chunk of cash ready to invest. Now what? You’re at a classic fork in the road: go all in at once (lump sum investing) or ease your way in over time using dollar cost averaging? This isn't just some technical finance question—it's a strategic choice that pits raw numbers against your own stomach for risk.

On paper, the math nerds will tell you lump sum usually wins. Markets, over the long haul, tend to go up. Getting your money into the game right away gives it the most time possible to ride that upward wave. Every day you wait on the sidelines is a day you could be missing out on gains.

But there's a huge "if" attached to that advice. The all-in approach works best if you don't happen to invest the day before the market decides to take a nosedive. Lump sum is the higher-risk, potentially higher-reward play. Get the timing right, and you're golden. Get it wrong, and you're starting deep in the red.

The Trade-Off Between Returns and Risk

This debate isn't about finding the one "best" strategy. It's about finding the one that fits you—your finances and, just as importantly, your personality. DCA is, at its heart, a risk-management tool. It's designed to give you peace of mind by smoothing out your entry point and saving you from the gut-wrenching regret of a badly timed, all-in bet.

Here’s a simple way to think about it:

- Lump Sum Investing: This is all about maximizing your time in the market. Statistically, it's a powerful move, but it leaves you totally exposed to short-term market swings.

- Dollar Cost Averaging: This is about minimizing the pain of bad timing. It acts as an emotional safety net when markets drop, but you might give up some potential gains for that comfort.

The right answer depends on how you feel about that trade-off. Can you handle the thought of a big, immediate drop for a shot at better long-term returns? Or do you sleep better at night knowing you're easing in, protected from the nightmare of buying at the absolute peak?

The decision between DCA and lump sum investing is a personal one, balancing the historical data favoring lump sum with the psychological and risk-mitigation benefits of a gradual approach.

What the Data Says About Both Strategies

Research gives us some hard numbers to work with here. A major study looked at four decades of market data and found something fascinating. Investors who used DCA, even if they started at a market peak, still managed to pull in a solid 10.4% average annualized return over 10 years. That’s a bit less than the 11.7% return for lump sum investors who got in under normal conditions, which shows what you might miss by waiting. You can dig into the full study to learn more about the long-term performance of both strategies.

But here's the kicker. What happened when lump sum investors got their timing horribly wrong? When they tried to time the market and ended up buying right at a peak, their average returns cratered to just 8.3%.

This data frames the decision perfectly. Lump sum investing tends to come out on top when markets are behaving normally. But dollar cost averaging is your safety net. It delivers strong returns while shielding you from the worst-case scenario—investing a huge pile of cash at the worst possible moment. Think of it as an insurance policy against really bad luck.

When Does Dollar Cost Averaging Make the Most Sense?

Dollar cost averaging isn't some abstract theory you read about in a finance textbook. It's a real-world tool that shines in a few very specific situations. Knowing when to pull this strategy out of your toolbox can make a huge difference, not just for your portfolio's growth but for your own peace of mind.

For anyone just getting started, DCA is a game-changer. The fear of investing a big chunk of cash at the "wrong time" is real, and it keeps a lot of people sitting on the sidelines. DCA sidesteps that paralysis by breaking your investment into smaller, more manageable pieces. You get your money into the market without the anxiety of one big, all-or-nothing decision.

You've Got a Windfall—Now What?

Getting a large, unexpected sum of money is a great problem to have, whether it’s from an inheritance, a big bonus, or selling a property. But it also creates a challenge. Your first instinct might be to invest it all at once to get it working for you, but that move exposes you to massive timing risk.

This is a perfect scenario for dollar cost averaging.

Instead of going all-in, you can feed the windfall into the market over several months or even a year. This smooths out your purchase price and protects you from the nightmare of investing your entire sum right before a market dive. It’s a methodical approach that helps you navigate potential volatility.

This is more relevant than ever. The United States is in the middle of a massive wealth transfer, with an estimated $70 trillion expected to change hands over the next 25 years. Many people will suddenly face the question of how to invest new capital wisely. You can discover more insights about managing a windfall on vaneck.com.

The Strategy You're Probably Already Using

Here’s a little secret: millions of people are already using dollar cost averaging, many without even knowing it. If you contribute to a 401(k), 403(b), or another workplace retirement plan, you’re a DCA pro.

Every time a slice of your paycheck is automatically invested, you're practicing dollar cost averaging. A fixed amount of your money buys shares of your chosen funds, whether the market is soaring or dipping. That automated, consistent process is the heart of DCA.

This really gets to the core strength of the strategy. It’s all about building discipline and consistency—two of the most critical habits for successful long-term investing.

Of course, a good strategy needs a solid framework. It’s always a good idea to review some portfolio management best practices for 2025 to make sure your overall approach is sound. Whether you're a new investor, managing a windfall, or just contributing to your 401(k), DCA provides a clear, structured path to building wealth.

Putting Dollar Cost Averaging into Action

Alright, enough with the theory. Let's get practical.

Putting a dollar cost averaging strategy into motion is surprisingly simple. This isn't about becoming a market analyst overnight; it's about setting up a routine you can actually stick to. You can break it all down into a few easy steps that keep your eye on the prize: your long-term goals.

Your first move involves just two decisions: how much to invest, and how often. You don't need to start with a huge amount. In fact, consistency beats a big starting number every time. Committing to something like investing $200 on the 15th of every month is a fantastic starting point.

Next up, you have to decide what to invest in. For DCA to work its magic, you'll want to look at broadly diversified, low-cost options.

Selecting and Automating Your Investments

Think about assets that give you a slice of the entire market. This helps you capture overall growth while spreading your risk around so one company’s bad day doesn’t tank your portfolio. A few solid choices for this approach include:

- Index Funds: These are a classic for a reason. They track a major market index, like the S&P 500, giving you instant diversification without the headache of picking individual stocks.

- ETFs (Exchange-Traded Funds): Very similar to index funds, ETFs are essentially baskets of stocks or bonds that you can buy and sell just like a single stock.

Once you’ve picked your investments, the last step is the most important one: automation. Log into your brokerage account and find the option to set up a recurring investment plan. This "set it and forget it" move is the secret sauce.

Automation is what makes DCA powerful. It locks in your discipline, shielding you from the temptation to react to scary headlines or your own emotions. It’s what keeps you on track when the market gets chaotic.

By automating your contributions, you turn investing from a series of high-stress decisions into a quiet, background habit that just works. To really nail down your own system, check out our guide to master the investment decision-making process for smarter investing. It’ll help you build wealth methodically, without the guesswork.

Got Questions About Dollar Cost Averaging?

Even once the concept of dollar cost averaging clicks, a few practical questions almost always pop up. Let's run through the most common ones so you can start using this strategy with confidence.

What if the Market Only Goes Up?

This is a great question and a totally valid concern. If you kick off a DCA plan right as the market starts a long, steady climb, you'd definitely have made more money by investing a lump sum at the very beginning. It's simple math—your regular buys will get you fewer and fewer shares as prices rise, pushing your average cost higher than if you'd gone all-in from day one.

But here’s the thing: nobody has a crystal ball. DCA is fundamentally a risk-management play. You're intentionally trading the potential for hitting the absolute jackpot in a bull run for solid protection against the risk of dumping your cash in right before a nosedive.

Think of dollar cost averaging less as a tool for chasing the highest possible return, and more as a disciplined, stress-free way to get into the market that takes the guesswork out of timing.

Is DCA a Good Idea for Individual Stocks?

You can use DCA for single stocks, but it’s a much better fit for broadly diversified investments like index funds or ETFs. Why? Individual stocks come with what’s called company-specific risk. If that one company hits a rough patch and its stock price tanks, it might never bounce back. Your DCA strategy would just be throwing good money after bad.

When you DCA into a broad market fund, you're not betting on a single company's fate. You're betting on the long-term growth of the entire economy, which is a much safer and more reliable proposition over time. DCA and diversification are a powerful combination.

How Long Should I Spread My Investments Out?

This really depends on the amount you're investing and your own comfort level with risk. For a large, one-time sum like an inheritance or a bonus, a common timeframe is somewhere between 6 and 12 months.

That window is usually long enough to smooth out any wild short-term swings without leaving too much of your money sitting on the sidelines, getting eaten by inflation. But your personal risk tolerance is the most important factor. If you're a nervous investor, stretching it to 18 months might help you sleep better. If you're more aggressive, you might shorten it to just three.

At Fear Greed Tracker, we arm you with the market sentiment data needed to make smarter decisions, whether you're using DCA or any other strategy. Check out real-time Fear & Greed scores to get a feel for the market's mood and refine your investment approach at https://feargreedtracker.com.