When you hear "investment process," it might sound intimidating, like something reserved for Wall Street pros in slick suits. But really, it's just a structured way to make smart money moves. It's the difference between gambling on a hot tip from a friend and building a disciplined strategy that can actually create wealth over the long haul.

Understanding the Foundation of Smart Investing

Investing without a plan is like setting sail without a map. Sure, you'll end up somewhere, but it’s probably not where you wanted to go. A solid investment decision making process is your personal roadmap, designed to keep you on course through both calm and turbulent market waters. It’s the one thing that stands between emotional, knee-jerk reactions and rational, strategic choices.

This isn't some secret formula. It's just a logical sequence of steps anyone can follow. The whole idea is to stop guessing and start being methodical. By setting clear rules and goals for yourself upfront, you build a powerful defense against all the market noise and common behavioural traps, like panic selling during a downturn or chasing some over-hyped stock that's all over the news.

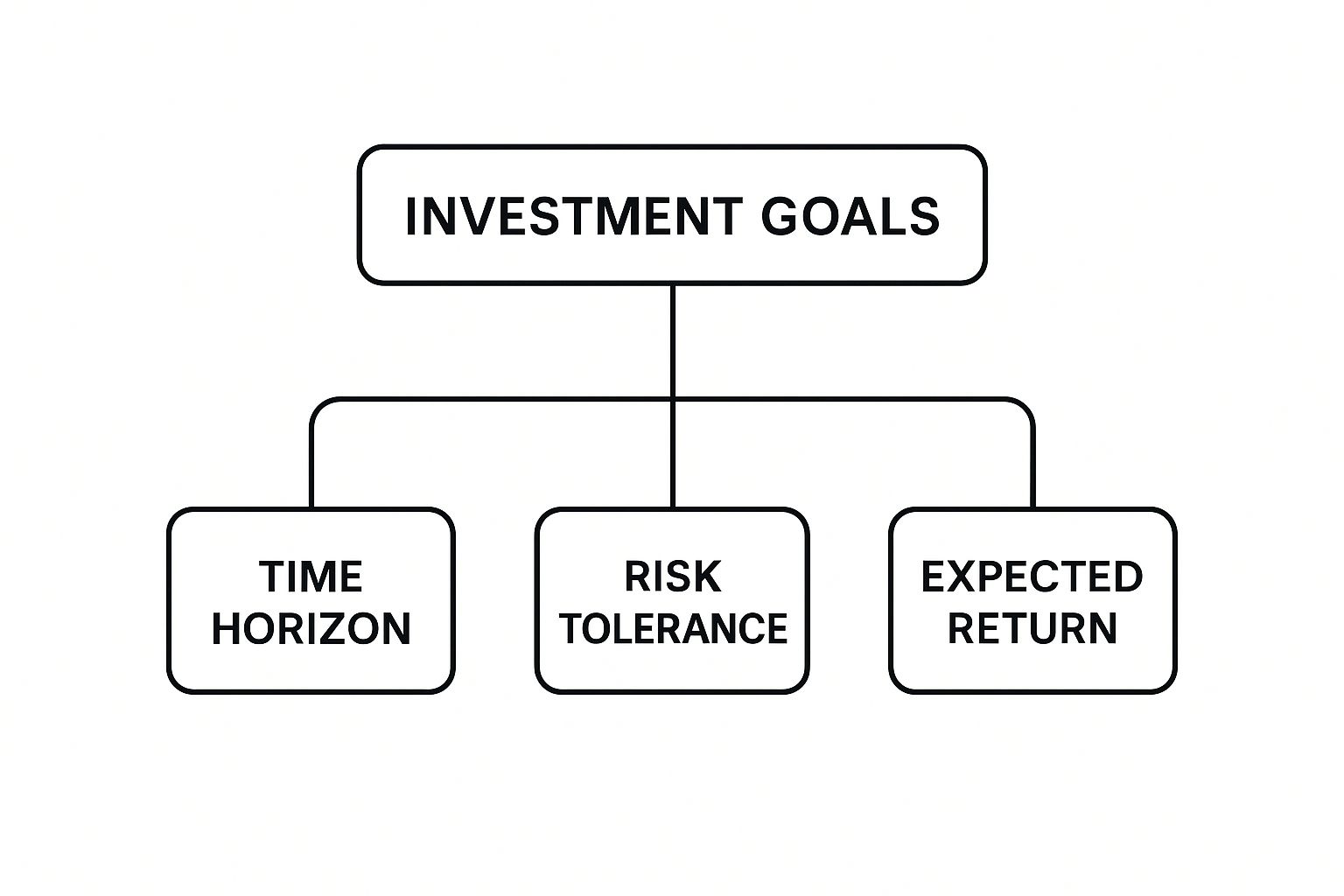

The Three Pillars of Your Investment Goals

Everything starts with your goals. What are you actually trying to achieve with your money? From there, everything else falls into place, guided by three interconnected pillars.

- Time Horizon: This is simply how long you have before you need the money back. A recent grad saving for retirement has decades to work with. Someone saving for a house down payment in three years has a much shorter runway.

- Risk Tolerance: How much turbulence can you stomach? An aggressive investor might be okay with big swings in their portfolio's value for a shot at higher returns. A conservative investor, on the other hand, is going to prioritize protecting their initial capital above all else.

- Expected Return: This is the growth you need to hit your goals. It has to be realistic and sync up with your risk tolerance and time horizon. You can't expect a 20% return with zero risk—it just doesn't work that way.

This diagram shows you exactly how these three components branch out from your main investment goals.

As you can see, your goals are the anchor. They dictate how you should think about risk, time, and returns. These pieces aren't separate, either—they all influence each other. For instance, a long time horizon usually means you can afford to take on a bit more risk.

The 5 Core Stages of Investment Decision Making

To bring this all together, the process can be broken down into five clear stages. Think of it as a repeatable cycle that keeps your strategy sharp and aligned with your objectives.

| Stage | Primary Objective | Key Activities |

|---|---|---|

| 1. Setting Goals | Define what you want to achieve financially. | Determine time horizon, risk tolerance, and required returns. |

| 2. Analysis | Evaluate potential investment opportunities. | Research assets, analyze market sentiment, and perform due diligence. |

| 3. Selection | Choose specific investments for your portfolio. | Pick stocks, bonds, or funds that match your analysis and goals. |

| 4. Allocation & Diversification | Build a balanced and resilient portfolio. | Decide how much to invest in each asset and spread risk. |

| 5. Review & Rebalance | Maintain and adjust your portfolio over time. | Monitor performance, review goals, and sell/buy assets as needed. |

Following these stages ensures you're not just making random bets but are instead building a cohesive, goal-oriented portfolio.

A well-defined process is the only reliable way to ensure that once a decision is made, you have the right structure and support to implement it effectively. It turns a good idea into a successful outcome.

Ultimately, having a strong investment process gives you the confidence to act. It helps you analyze opportunities, build a portfolio that can weather storms, and make adjustments based on a clear strategy, not fear. It’s what separates the passenger being tossed around by market waves from the captain who is charting a steady course toward their financial destination.

Defining Your Personal Investment Roadmap

Before you even think about analyzing a single stock or bond, you need a map. Seriously. The most critical step in the entire investment decision making process is figuring out your personal investment roadmap.

Think of it like planning a cross-country road trip. You wouldn't just jump in the car and start driving without knowing where you're going, how much you can spend on gas, or whether you want to take the fastest highway or the scenic backroads. Investing is no different.

This first stage is all about you. It moves past generic advice and forces you to lay a foundation that every single one of your future choices will rest on. It’s where you define your "why," which in turn tells you "how."

Setting Specific and Measurable Goals

Your financial goals are the destinations on your map. Vague dreams like "I want to be rich" don't work because you can't act on them. You need concrete, measurable targets with clear deadlines.

A great way to set goals is to get incredibly specific. Instead of "saving for a house," a much better goal is "saving $50,000 for a down payment on a home in the next five years." Right away, this clarifies two essential pieces of the puzzle: your target amount and your time horizon.

Your goals will likely fall into a few buckets:

- Short-Term (1-3 years): Maybe you're saving for a new car or that big vacation you've been dreaming of.

- Mid-Term (3-10 years): This could be for a house down payment or funding a child's education.

- Long-Term (10+ years): This is the big one—building a nest egg for retirement or reaching total financial independence.

Each of these goals demands a completely different strategy. You wouldn't invest your house down payment money the same way you’d invest your retirement funds. Why? The time you have to bounce back from any potential losses is worlds apart.

Uncovering Your Investment Philosophy

Okay, so you know your destination and your timeline. Now it's time to figure out your travel style. This is your investment philosophy—a personal set of beliefs and principles that will guide you, especially when the market gets chaotic. It’s mostly shaped by how much risk you can stomach and what you value.

Your investment philosophy is your constitution. It's the document you turn to when markets are chaotic and emotions are running high, reminding you of the rules you set for yourself when you were thinking logically and clearly.

To build this philosophy, you have to be brutally honest about your risk tolerance. Does the idea of big portfolio swings in exchange for potentially higher returns excite you? Or does the thought of losing money keep you up at night? There’s no right or wrong answer, only what’s right for you.

Your time horizon plays a huge role here. An investor with 30 years until retirement can afford to take on way more risk than someone who needs their cash in two years.

Lately, personal values have become a huge part of this conversation. Environmental, Social, and Governance (ESG) criteria are no longer some niche interest; they are central to how a lot of people invest. A stunning 89% of investors now consider ESG factors, with projections suggesting these assets will climb to nearly $35 trillion globally. If you want to see just how much values are shaping decisions, you can check out more ESG statistics.

This might mean your philosophy includes avoiding certain industries or actively looking for companies that align with your ethics.

By clearly defining your goals, time horizon, risk tolerance, and personal values, you create a solid roadmap. This framework is your best defense against making emotional mistakes and ensures every step you take is a deliberate move toward your financial destination.

How to Find and Analyze Investments

Okay, you’ve got your personal roadmap. Now it’s time to find the right vehicle to get you where you want to go. This is where we shift our focus from our own goals to the wider market, hunting for and sizing up potential opportunities.

This isn’t about throwing darts at a board; it’s about becoming an investigator. Your job is to gather the evidence, check the facts, and make a solid call on an asset’s potential. There are two main ways to do this: fundamental analysis and technical analysis. And no, they’re not enemies. They’re actually two sides of the same coin in a smart investor’s pocket.

Understanding Fundamental Analysis

Think of fundamental analysis as being a detective for a specific business. Your mission is to figure out what a company is really worth. To do that, you'll need to dig into its financial health, the quality of its leadership, its competitive edge, and the state of its industry.

You’re really just trying to answer one big question: Is this a solid, well-run company that the market is pricing fairly?

To get your answer, you’ll be looking at a few key things:

- Financial Statements: These are basically the company's report cards. You'll want to look at the income statement (how much money it's making), the balance sheet (what it owns vs. what it owes), and the cash flow statement (how cash is actually moving in and out).

- Key Ratios: Metrics like the Price-to-Earnings (P/E) ratio, Debt-to-Equity ratio, and Return on Equity (ROE) are your best friends for comparing a company against its rivals or its own past performance.

- Qualitative Factors: This is the stuff that doesn't fit neatly into a spreadsheet, like how strong the brand is, how experienced the management team is, and where it sits in the competitive landscape.

This whole approach is about understanding the "what" and the "why" behind an investment. It’s a long-term game focused on the quality of the business, not just the little price wiggles that happen day to day.

"I find audit transparency critical to assessing a company’s financial health. CAMs can reveal the most complex or judgmental areas of an audit, which helps me identify potential risk points."

That insight shows just how deep fundamental analysis can go. It’s no surprise that nearly all institutional investors—a whopping 93%—read the Critical Audit Matters (CAMs) section in company filings to spot these potential red flags.

Decoding Technical Analysis

If fundamental analysis is playing detective, then technical analysis is more like being a market psychologist. It’s all about studying price charts and trading volumes to spot patterns and trends. The core belief here is that all the important information is already baked into an asset's price, and that human behavior tends to create patterns you can actually predict.

Instead of digging through a company’s financials, a technical analyst uses tools like:

- Moving Averages: These smooth out the choppy price data to help you see the underlying trend more clearly.

- Relative Strength Index (RSI): This handy indicator helps you figure out if an asset is getting overbought (too expensive, too fast) or oversold (a potential bargain).

- Support and Resistance Levels: These are specific price points where an asset has historically struggled to break through (resistance) or fall below (support).

Technical analysis is really focused on the "when" of investing—helping you time your entries and exits based on what the market mood and momentum look like right now. It's especially useful for shorter-term trading.

Using Data in Today's Market

Let’s be honest: today’s market is flooded with data, which opens up entirely new ways to analyze everything. Technology has completely changed how we find opportunities, especially when you look beyond the public stock market.

Tech innovation and what investors are looking for have had a huge impact on the investment decision-making process. For instance, AI-native startups recently pulled in almost half of all global venture capital money. This points to a massive focus on tech and healthcare, which 47% of Limited Partners (LPs) see as the hottest opportunities out there. You can read more about these evolving investor priorities to get a sense of how new ideas are shaping where the money flows.

At the end of the day, a balanced approach is usually your best bet. Use fundamental analysis to figure out what to buy—strong companies at a fair price. Then, bring in technical analysis to help decide when to buy, using market sentiment to nail a better entry point. By combining both, you build a powerful framework for analyzing any investment and gain the confidence to make your move.

Building a Resilient Investment Portfolio

Here's a hard truth: successful investing is almost never about hitting a home run on one magical stock. It’s far more like building a championship sports team—a well-rounded group of assets that work together, balancing each other’s strengths and weaknesses to help you win over the long haul.

This part of the investment decision making process is where you stop being a spectator and become the architect of your own financial future. Your job is to construct a portfolio that can weather the inevitable market storms.

The guiding principle is as simple as it is timeless: don't put all your eggs in one basket. This is the heart of diversification, and it's your single best defense against unexpected market shocks.

The Power of Diversification

Think of your portfolio like that championship team. You wouldn’t send out five star strikers and hope for the best; you need defenders, midfielders, and a solid goalie. Each player has a distinct role, and their combined skills make the team adaptable enough to take on any opponent.

Investing works the same way. It's about spreading your capital across different types of assets that react differently to the same economic news. When one part of your portfolio zigs, another part might zag, which helps smooth out your overall returns and lets you sleep better at night.

For diversification to really work, you need to think in layers:

- Asset Classes: This is your foundation. A healthy mix of stocks (for growth), bonds (for stability and income), and alternatives like real estate or commodities creates a sturdy base.

- Industries and Sectors: Don't just own stocks—own stocks across different fields. Having money in technology, healthcare, and consumer goods means a downturn in one sector won't sink your whole ship.

- Geographic Regions: Look beyond your home country. Investing in both established and emerging markets can shield you from a domestic slump and unlock completely new avenues for growth.

This multi-layered defense is how you build a portfolio that’s resilient by design.

Choosing Your Asset Allocation Model

Once you're sold on why you need to diversify, the next question is how. This is where asset allocation comes in—it’s simply the percentage of your portfolio you put into each asset class. This single decision will likely have a bigger impact on your long-term results than any individual stock you pick.

Your ideal allocation isn't a one-size-fits-all formula. It flows directly from the personal roadmap you've already built: your goals, your timeline, and how much risk you’re truly comfortable with.

A well-chosen asset allocation acts as your portfolio’s internal shock absorber. It’s what allows you to stay invested through market volatility, turning potential panic into a manageable part of the journey.

To get you started, here are a few classic models:

| Model | Typical Stock/Bond Mix | Best For |

|---|---|---|

| Aggressive Growth | 80% Stocks / 20% Bonds | Young investors with a long time horizon and high risk tolerance. |

| Moderate Growth | 60% Stocks / 40% Bonds | Investors seeking a balance of growth and stability, often in their peak earning years. |

| Conservative | 40% Stocks / 60% Bonds | Investors nearing retirement who prioritize protecting their capital over chasing high returns. |

Treat these as starting points, not rigid rules. The goal is to find a mix that lets you stay the course without losing sleep, while still giving your money the chance to grow. And don't forget that managing these assets comes with costs. To get a better handle on this, check out our guide to understand asset management fees and save more on investments.

A quick look at recent market trends shows just how important this is. We've seen major indexes like the S&P 500 become heavily concentrated in a few giant tech companies. This kind of concentration risk can lead to more volatility, making smart portfolio construction and risk management more critical than ever.

Of course. Here is the rewritten section, crafted to sound like it was written by an experienced human expert, following all the provided guidelines.

How to Manage and Adjust Your Portfolio

So, you’ve built your portfolio. Great. But the work isn't over—in fact, it’s just getting started. The final, and arguably most important, part of the investment decision making process is the ongoing care and feeding of your portfolio. This keeps your strategy aligned with your actual goals over the long haul.

This isn't about gluing your eyes to the screen and sweating every daily market dip. It's about a disciplined, scheduled check-in to make sure your asset allocation hasn't wandered off course. As time goes on, some investments will inevitably grow faster than others, knocking that perfect balance you created out of alignment. That's where a simple but powerful technique called rebalancing comes in.

The Discipline of Rebalancing

Rebalancing is just what it sounds like: systematically steering your portfolio back to its original target. It's a way to enforce one of investing's oldest and wisest rules: buy low and sell high.

The process is refreshingly simple. You sell off a small slice of the assets that have done really well (selling high) and reinvest that money into the assets that have lagged behind (buying low). I know, it can feel wrong—why would you ever sell your winners? But think of it as a critical risk management tool. It stops you from becoming dangerously over-invested in a single hot area and keeps your portfolio locked in on your personal risk tolerance.

There are a couple of common ways to do this:

- Time-Based Rebalancing: This is the set-it-and-forget-it method. You pick a schedule—maybe quarterly, every six months, or once a year—and you rebalance on that date, no matter what the market is doing.

- Threshold-Based Rebalancing: This approach is a bit more hands-on. You only rebalance when an asset class drifts by a certain amount, like 5% or 10%, from its target. It can be more efficient but means you have to keep a closer eye on things.

No matter which method you choose, rebalancing is the foundation of good portfolio hygiene. It injects discipline into your process, taking raw emotion out of the equation and forcing you to stick to the smart plan you made with a clear head.

Using Sentiment as a Guide, Not a Trigger

While rebalancing is mostly a mechanical task, true portfolio management also means having a feel for the market’s psychological climate. This is where a tool that measures market sentiment, like a Fear & Greed Index, becomes incredibly useful. The idea isn't to use these scores as a panic button for buying or selling, but to add a layer of context to the decisions you're already making.

A sentiment gauge gives you a quick read on whether the market is running on logic or pure emotion. For example, the CNN Fear & Greed Index boils down seven different indicators to show you what's really driving market behavior.

This reading gives you an immediate visual cue of the market's mood. It helps you understand the "why" behind the price charts. Is that recent rally built on solid fundamentals, or is it just irrational hype? Is a big sell-off a sign of real trouble, or is it just widespread panic?

By understanding the emotional state of the market, you can better contextualize your rebalancing decisions. It gives you the confidence to act when others are fearful and to be cautious when others are greedy.

When the index is screaming "Extreme Fear," it might be a sign that investors are overly pessimistic. For a long-term investor, that could signal a great buying opportunity during your scheduled rebalance. On the flip side, a reading of "Extreme Greed" could suggest the market is getting frothy, making it a smart time to trim those overvalued positions, just as your rebalancing strategy dictates. This approach helps you make calm, data-informed adjustments instead of emotionally-driven, costly mistakes.

Making Sense of Market Noise and Economic Trends

Headlines are designed to grab your attention. Markets swing wildly, and fear is a powerful motivator—and a great way to sell news. A huge part of any solid investment decision making process is learning how to filter out this daily "noise" and focus on the signals that actually move the needle.

It’s all about seeing the bigger picture, looking past the short-term panic that the 24-hour news cycle thrives on. Smart investors don’t see major economic forces as random threats. Instead, they treat them as the predictable currents they need to navigate to reach their destination. These are the large-scale trends that can genuinely impact your portfolio over months and years, not just minutes or hours.

Identifying the True Market Movers

A single tweet from a celebrity might cause a stock to flicker for a day, but there are two forces with the power to shift the entire market for the long haul: inflation and interest rates. Getting a handle on how these two work is non-negotiable for making sound, lasting investment decisions.

Inflation: Picture inflation as a slow, steady leak in your financial tire. When it’s running high, the cash in your pocket and the returns you earn are simply worth less over time. It puts the squeeze on companies by driving up their costs for everything from raw materials to employee salaries, which can seriously dent their profits.

Interest Rates: Think of these as the gas and brake pedal for the entire economy. When the central bank hikes rates to combat inflation, it gets more expensive for everyone—companies and consumers alike—to borrow money. This naturally slows down economic growth, creating a headwind that can weigh down the stock market.

The two are locked in a constant dance. Central banks will often raise interest rates with the specific goal of taming inflation, creating a delicate balancing act that sends ripples through every corner of the financial world.

Navigating the Global Economic Landscape

Today's markets are more connected than ever. A factory shutdown in Asia, a new policy in Europe, or a resource discovery in South America can have a direct impact on your portfolio right here at home. This global web creates both unique risks and incredible opportunities.

For example, major economic reports consistently show how these global pressures shape what investors do. In one recent survey, inflation was named the top challenge by 86% of institutional investors, with interest rate risks right behind at 83%. Yet, despite these headwinds, sentiment is still surprisingly upbeat. A majority of investors (62%) still view North America and Europe as the best places to invest. You can explore more insights from the global investor survey to see how the pros are thinking.

When you start seeing the market through the lens of economic trends, you can finally base your decisions on strategy, not on fear. You go from being a passenger tossed around by the waves to a captain charting a clear course through them.

By focusing on these big-picture trends, you give yourself the context to understand the daily news. Is a market dip just a knee-jerk reaction to a fleeting headline, or is it part of a broader economic slowdown you’ve been tracking? Having that perspective is critical. If you want to sharpen this skill, it’s worth your time to learn more about using the Stock Fear and Greed Index to your advantage, as it adds another powerful layer of data on market psychology.

Ultimately, this approach helps you stay disciplined, filter out the noise, and act only on the signals that align with your long-term plan.

Common Questions About the Investment Process

Even with a solid game plan, turning theory into action can feel a bit uncertain. Let's walk through some of the most common questions that pop up when investors start applying these principles. Getting these points straight helps build the confidence you need to get in the game and stick with your strategy.

How Often Should I Review My Investment Portfolio?

For most long-term investors, a deep dive once or twice a year is plenty. That’s enough time to rebalance your assets and make sure your portfolio is still tracking toward your financial goals, without getting obsessive about it.

It's easy to fall into the trap of checking your portfolio daily or even weekly. This is a classic mistake. It often leads to emotional, knee-jerk decisions based on normal, everyday market noise instead of your long-term vision. The idea is to monitor progress, not micromanage every little price swing.

What Is the Biggest Mistake New Investors Make?

Without a doubt, the most common—and most expensive—mistake is skipping the groundwork. So many new investors jump straight to buying whatever’s hot, whether it's a buzzy stock or the latest crypto trend. They do this without ever defining their goals, figuring out their risk tolerance, or building an investment philosophy.

This kind of reactive, unstructured approach almost never pays off in the long run. Without a personal roadmap to guide them, they’re easily swayed by market hype, panic selling, and end up with a portfolio that doesn't actually fit their needs.

A downturn is the ultimate test of your process. If you set your goals and risk tolerance correctly from the start, the best move is often to stick to the plan you made when you were thinking clearly and logically.

How Do Market Sentiment and Economic Trends Fit In?

This is where you can really sharpen your edge. Understanding market sentiment gives you the context behind the numbers. It helps you see whether price moves are driven by solid fundamentals or by widespread fear or greed. If you want to go deeper, you can check out our guide on what market sentiment is and how to measure it. This insight is gold when you're navigating a tricky economic climate.

For example, look at the private credit market. It has swelled to $1.6 trillion in assets under management, a massive figure that shows just how complex the landscape has become. To learn more, you can discover more insights about private market trends. Staying on top of these big-picture trends isn't just "nice to have"—it's a critical part of a sophisticated investment process.

Ready to stop guessing and start making data-driven decisions? The Fear Greed Tracker gives you real-time sentiment scores on over 50,000 assets, empowering you to see the market's true mood. Take control of your investment process by visiting https://feargreedtracker.com today.