Portfolio rebalancing is the secret sauce to keeping your investment strategy on track. It’s the simple, disciplined act of buying and selling assets to bring your portfolio back to its original target mix. Think of it as a periodic tune-up for your investments, making sure you don't accidentally swerve off the road to your financial goals.

What Is Portfolio Rebalancing Anyway?

Imagine you’ve planted a garden with a specific design in mind. You decided on 60% flowers (stocks) for their beautiful growth potential and 40% vegetables (bonds) for their steady, reliable harvest.

After a fantastic growing season, the flowers have absolutely exploded. They’ve grown so much that they now take up 75% of your garden. Your carefully planned balance is gone, and your garden is now much more vulnerable to a single bad season for flowers.

Portfolio rebalancing is just like getting out the pruning shears. You trim back the overgrown flowers and plant more vegetables to get back to that original 60/40 layout.

The Problem of "Portfolio Drift"

When you don't do this kind of maintenance, your portfolio starts to "drift." This is what happens when one type of asset—like stocks—grows much faster than another, completely changing your portfolio's risk profile without you even noticing. What was once a balanced plan can quietly become a high-risk, aggressive one, leaving you overexposed when the market eventually takes a downturn.

Rebalancing is a brilliant way to take emotion out of the equation and force yourself to follow the timeless wisdom of investing: "buy low, sell high."

By selling some of the assets that have done really well, you’re locking in your profits. Then, you take that cash and reinvest it into the assets that have been lagging, buying them while they're cheap.

This isn't about timing the market; it's about sticking to your plan. It’s a systematic process that keeps you grounded instead of reacting to every bit of sensational news or market panic. In fact, research covering two decades shows that global investors consistently trim their winning equities to get their risk-return balance back in line. You can explore the detailed findings on how investors manage their portfolios across global markets.

Let's see how this works with a simple table.

How Portfolio Drift Changes Your Plan

This table shows how a simple 60/40 portfolio can drift away from its target and how rebalancing snaps it back into place.

| Asset Class | Your Target Mix | Mix After Market Growth | Mix After Rebalancing |

|---|---|---|---|

| Stocks | 60% | 70% | 60% |

| Bonds | 40% | 30% | 40% |

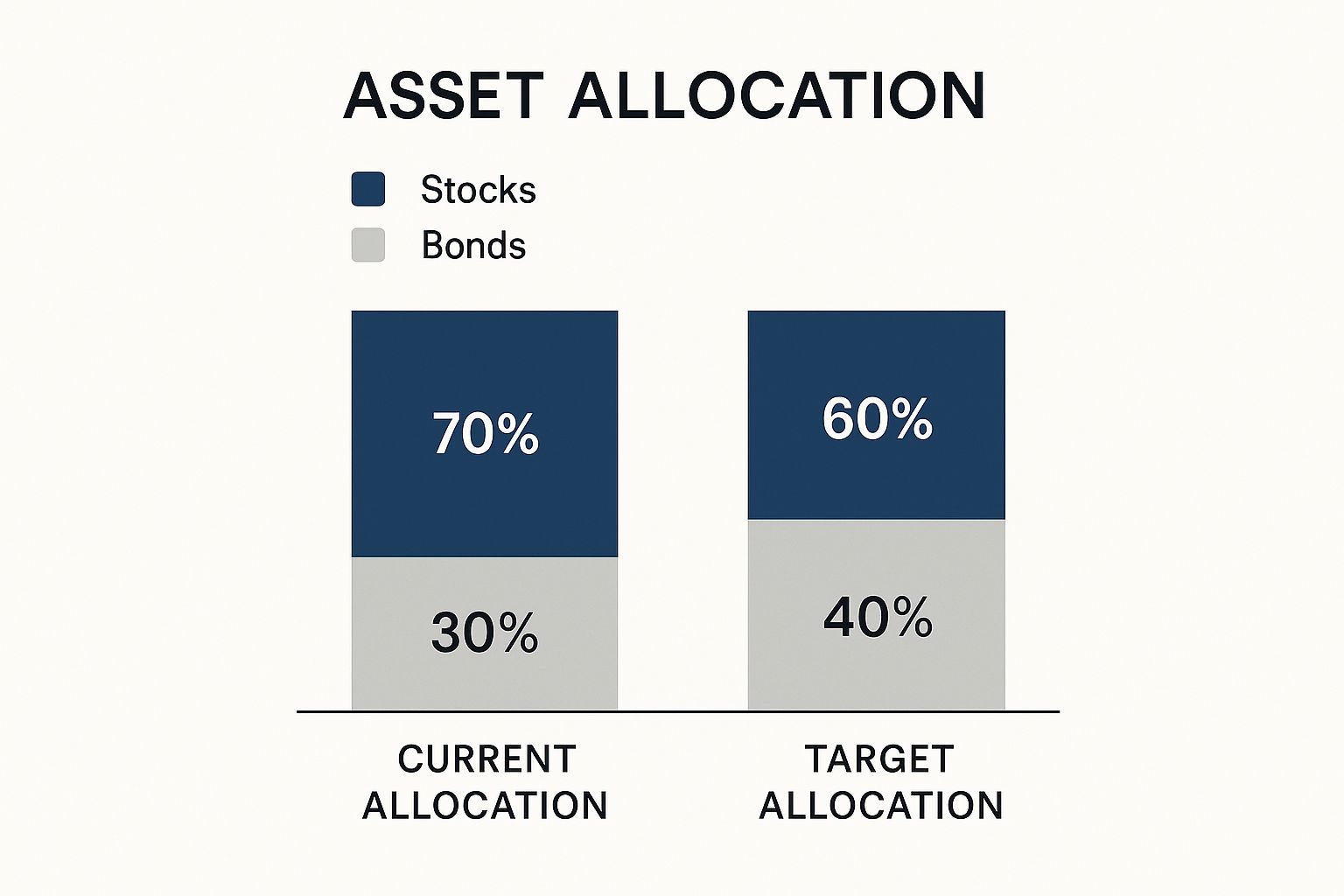

As you can see, after a strong run in stocks, your portfolio became riskier than you intended. Rebalancing simply means selling 10% of your stocks and buying 10% more bonds to restore your original, comfortable risk level.

Ultimately, getting a handle on rebalancing is the first big step toward building a more resilient, goal-focused investment strategy. It’s the discipline that keeps your long-term vision clear, no matter what the markets are doing day-to-day.

Why Rebalancing Is Your Best Defense Against Risk

Without regular check-ups, even the most carefully crafted portfolio can drift into dangerous territory.

Picture this: you decide on a moderate risk level for your investments, aiming for a 60% stock allocation. But after a roaring bull market, you look again and find that stocks now make up 80% of your portfolio. Sure, the high returns feel great, but you’re now taking on way more risk than you ever intended.

This "portfolio drift" quietly turns a balanced strategy into a high-risk gamble. When a market downturn eventually hits—and it always does—your overexposed portfolio is set up to suffer much larger losses than you planned for. It’s like sailing a ship meant for calm waters straight into a storm; you're simply not prepared for that kind of volatility.

Aligning Investments with Your Life Goals

Rebalancing is about more than just tweaking percentages. It’s about making sure your investments stay locked in on your real-world financial goals.

Your strategy for a retirement that's two decades away should look completely different from a plan to save for a house down payment in three years. As you get closer to those big life moments, your tolerance for risk naturally goes down.

Letting your portfolio drift means your investments might no longer fit your timeline or life circumstances. Rebalancing acts as a crucial guardrail, preventing that unintended risk and keeping you firmly on the path you originally set. It’s a core discipline that separates hopeful speculation from strategic investing. To go deeper, you can explore some of the best practices for risk management in 2025 to further protect your assets.

The Hidden Discipline of Selling High and Buying Low

One of the biggest, and often overlooked, benefits of rebalancing is that it builds an automatic, emotion-free system to "sell high and buy low." The whole process forces you to take action based on a plan, not on market hype or gut-wrenching fear.

Let’s break it down:

- Stocks are soaring: Your rebalancing schedule tells you it's time to sell some of your top-performing stocks, locking in profits while prices are high.

- Bonds are lagging: You then take those profits and use them to buy more of your underperforming assets (like bonds) at a lower price.

This systematic approach stops you from getting swept up in the euphoria during market peaks or panicking during downturns. Instead of chasing returns, you’re methodically trimming your winners and buying undervalued assets, which almost always leads to smoother, more predictable growth over the long haul.

Research has shown that when a crisis hits, investors become far more reluctant to swap safe assets for risky ones. They tend to hold on for dear life right when they should be buying. Rebalancing gives you the structure to push past that hesitation, making sure you stick to your strategy when it matters most.

Think of it as the steady hand that guides your portfolio through market turbulence, keeping your financial future on course.

Choosing Your Rebalancing Strategy

Alright, so you’re sold on why you need to rebalance. That’s the easy part. The real question is how you're going to do it. There's no single "best" way—it really boils down to your personality, how much you like to tinker with your portfolio, and what you’re trying to achieve long-term.

Let's walk through the two most common approaches. Think of them as different paths to the same destination: a portfolio that stays true to your original plan.

The Simplicity of Calendar Rebalancing

The most straightforward method is calendar-based rebalancing. It’s exactly what it sounds like: you pick a date on the calendar, and on that day, you check in and adjust your portfolio. It’s a classic “set it and forget it” strategy that builds great discipline.

You could choose to rebalance:

- Annually: A popular choice. Many people do this around their birthday or at the start of the new year.

- Semi-Annually: A solid middle ground, giving you a check-in every six months.

- Quarterly: This is for investors who want to keep a tighter rein on their allocations.

The beauty of this is its simplicity. You don't have to obsess over daily market swings; you just stick to your schedule. This is perfect if you're busy and prefer a disciplined, low-effort routine.

The image below gives you a clear picture of what happens when a portfolio drifts and why rebalancing is so necessary.

As you can see, after the market does its thing, the portfolio is suddenly heavier on stocks than intended, which cranks up the risk level without you even realizing it.

The Precision of Tolerance Band Rebalancing

If you’d rather be more responsive, then tolerance-band rebalancing might be your style. Instead of relying on the calendar, you set a trigger point—a "tolerance band"—for each asset. You only step in to rebalance when an asset drifts too far from its target.

For instance, say your target for stocks is 60%, and you set a 5% tolerance band. You’d only rebalance if your stock allocation climbed above 65% or dropped below 55%. This approach is much more dynamic because it reacts directly to market moves. It keeps you from over-trading when things are quiet but forces you to act when there's a significant shift.

This method requires a bit more monitoring, but it’s incredibly effective at managing risk when the market gets choppy. Big institutional investors often use this approach to keep their massive funds in line.

A lot of the time, this strategy works wonders when paired with a consistent investment plan. To get the full picture on that, check out our guide on what dollar-cost averaging is and how it works.

Comparing Rebalancing Strategies

So, which one is for you? The hands-off calendar approach or the more active tolerance-band method? This table breaks it down to help you decide.

| Feature | Calendar-Based Rebalancing | Tolerance-Band Rebalancing |

|---|---|---|

| Trigger | A specific date (e.g., quarterly, annually) | An asset's allocation drifting past a set % (e.g., 5%) |

| Effort Level | Low. "Set it and forget it." | Higher. Requires regular monitoring of your portfolio. |

| Best For | Busy, long-term investors who prefer a simple routine. | Hands-on investors who want to react to market shifts. |

| Pros | Simple, disciplined, and prevents emotional decisions. | More responsive to market volatility, potentially better risk control. |

| Cons | Might miss major market swings between scheduled dates. | Can lead to more frequent trading and requires more attention. |

Ultimately, there’s no wrong answer here. The best strategy is the one you can actually stick with for the long haul.

Rebalancing vs. Buy-and-Hold in the Real World

Theory is great, but how do these strategies actually hold up when the market gets wild? The whole debate between rebalancing and a simple "buy-and-hold" strategy really boils down to one thing: managing risk versus chasing the highest possible returns.

A buy-and-hold approach is as passive as it gets. You buy your assets and just let them ride the market waves, for better or for worse. When stocks are on a tear in a relentless bull market, this hands-off method often wins. You’re not selling your best performers, so your portfolio’s value can climb sky-high, easily outpacing a rebalanced portfolio that’s systematically trimming those exact same winners.

But the market isn’t a one-way street. That same hands-off approach that fuels incredible gains can also lead to devastating losses when the party ends.

Performance During Market Downturns

This is where rebalancing really earns its keep as a defensive play.

Picture this: your 60/40 portfolio has drifted to a much more aggressive 80/20 mix right before a nasty correction hits. A buy-and-hold investor is about to feel the full force of the stock market’s drop on a whopping 80% of their portfolio.

The investor who rebalanced, on the other hand, would have already sold off some of those high-flying stocks at their peak, moving that money into the safety of bonds. When the crash comes, they have far less exposure to the assets that are tumbling.

This simple act creates a few huge advantages:

- Smaller Losses: Your portfolio’s value doesn’t fall nearly as far, protecting your hard-earned capital.

- Faster Recovery: With less ground to make up, your portfolio can bounce back much more quickly once the market turns around.

- Psychological Stability: It's a lot easier to stick to your long-term plan when you see smaller losses instead of panic-selling at the absolute worst time.

A Disciplined Look at Historical Performance

The data shows that neither strategy is the undisputed champion in every single scenario. Digging into the history, buy-and-hold tends to do better during long, sustained market trends—both up and down. But if you zoom out and look at full market cycles, regular rebalancing almost always leads to smaller drawdowns and better risk management. You can discover more insights about these findings to see exactly how each strategy behaves under pressure.

The real goal of rebalancing isn't to beat the market every single year. It's to achieve better risk-adjusted returns over the long haul. It smooths out the ride and reduces that gut-wrenching volatility.

Ultimately, buy-and-hold might feel easier, but it leaves you completely exposed to the emotional and financial roller coaster of market cycles. Rebalancing gives you a disciplined, unemotional system to lock in profits, buy assets when they're on sale, and stay true to your original risk tolerance. For most long-term investors, that discipline is the real key to success.

Your Step-by-Step Guide to Rebalancing

Alright, we’ve covered the what, why, and how of rebalancing. Now it’s time to roll up our sleeves and actually do it. Think of this four-step guide as your practical checklist for getting your portfolio back on track.

Step 1: Review Your Target Allocation

First things first: before you touch a single investment, look at your original game plan. What was the target mix you set for yourself? Was it the classic 60% stocks and 40% bonds, or something tailored to your own goals?

Life changes, and so do markets. This is your moment to sanity-check that your target allocation still makes sense. Maybe you’re a few years closer to retirement and that old 70% stock allocation feels a little too aggressive now. It might be time to dial it back to 60%. This step ensures you’re aiming for a target that’s still right for you today.

Step 2: Assess Your Current Portfolio

Next, you need a clear snapshot of where things stand right now. It's time to calculate the current weight of each asset class in your portfolio. You can easily do this with a basic spreadsheet, or let the analysis tools on your brokerage platform do the heavy lifting.

Let's imagine your total portfolio is worth $100,000. After a quick review, you find:

- Your stocks have grown and are now worth $75,000.

- Your bonds are lagging a bit, sitting at $25,000.

This means your current allocation has drifted to 75% stocks and 25% bonds. This simple calculation gives you the hard data you need to see exactly how far you’ve strayed.

Step 3: Identify the Gaps

With your target and current numbers in hand, the next part is just simple math. You're just comparing the two to see which parts of your portfolio are overweight and which are underweight. This is where your rebalancing to-do list starts taking shape.

Let’s stick with our example:

- Target: 60% stocks / 40% bonds

- Current: 75% stocks / 25% bonds

It’s pretty clear what happened. Your stocks are 15% over their target, and your bonds are 15% underweight. To get back to your desired balance, you need to shift $15,000 out of stocks and into bonds.

Step 4: Execute the Trades

Finally, it’s time to act. You’ve got two main ways to pull this off, and your choice can make a big difference when it comes to taxes.

- Sell and Buy: The most direct route is to sell some of your overweight assets (in our case, stocks) and use that money to buy more of your underweight assets (bonds). It’s quick and effective, but it can trigger capital gains taxes if you’re doing this in a taxable brokerage account.

- Use New Contributions: A smarter, more tax-friendly way is to simply steer new money into your underweight asset classes. So instead of selling anything, you’d just use your next contribution to buy more bonds until the portfolio gets back to that 60/40 target.

If you’re rebalancing inside a tax-advantaged account like a 401(k) or an IRA, things are much easier. You can sell and buy without worrying about an immediate tax bill. Knowing this difference is key to rebalancing efficiently and keeping more of your money.

Using Market Sentiment to Guide Your Strategy

A disciplined rebalancing plan is your portfolio’s anchor in stormy seas. But what if you could use the market's own psychology as a tailwind? This isn’t about trying to time the market—it’s about adding a layer of context to the rebalancing decisions you already plan to make.

This is where tools like the Fear & Greed Index come in. Think of it as a barometer for the market's mood, telling you whether the crowd is acting out of sheer panic or irrational euphoria.

Interpreting Market Moods

The beauty of the index is that it often works best as a contrarian indicator.

When the market is paralyzed by "Extreme Fear," it’s often a sign that assets have been oversold and are potentially trading at a discount. For a disciplined rebalancer, this can be the perfect green light to buy those beaten-down assets with confidence while everyone else is running for the exits.

On the flip side, a state of "Extreme Greed" suggests the market is getting overheated and might be due for a reality check. This serves as a powerful confirmation to follow your plan, trim your winners, and take some profits off the table—especially when the fear of missing out (FOMO) is screaming at you to do the opposite.

The index gives you a simple, visual snapshot of where things stand.

A reading like this one, showing "Greed," suggests investors are feeling pretty optimistic. If your rebalancing schedule calls for selling some of your high-flyers, this sentiment can reinforce that you're making a sound decision.

By layering sentiment analysis over your strategy, you’re not changing your plan. You’re simply using market psychology to help you pull the trigger on your rebalancing decisions at opportune times.

This gives you a logical framework to lean on when emotions are running high. To see how else you can apply these ideas, check out our guide on how to use market sentiment analysis for trading.

Answering Your Top Rebalancing Questions

Rebalancing can feel a bit abstract at first. Let's clear up some of the most common questions investors ask so you can start putting this powerful strategy to work with confidence.

How Often Should I Rebalance My Portfolio?

There’s no magic number here, but most investors follow one of two popular schedules.

The first is calendar-based rebalancing. It’s simple and disciplined: you check your portfolio on a set schedule—say, once a year or every six months—and make adjustments. Easy to remember, easy to do.

The other approach is using tolerance bands. Instead of waiting for a specific date, you act when an asset class drifts too far from its target, maybe by 5%. This method is more responsive to market moves but requires you to keep a closer eye on things. Your best bet depends on your investing style, how much you pay in transaction fees, and frankly, how often you want to think about it.

Does Rebalancing Always Improve Returns?

Nope, and it's not really designed to. In a roaring bull market where stocks just keep climbing, a portfolio you never touch might actually outperform a rebalanced one for a while. Why? Because you'd just be riding that winning wave without trimming back.

The real job of rebalancing isn't to chase the highest possible returns. It's to manage risk and keep your investments locked on your long-term goals.

Over a full market cycle—including the inevitable ups and downs—rebalancing helps enforce a "buy low, sell high" discipline automatically, taking the emotion out of the equation. This often leads to better risk-adjusted returns in the long run.

What Are the Tax Implications of Rebalancing?

This is a big one. When you sell winning investments in a regular brokerage account, you can get hit with capital gains taxes. But you can be smart about it.

Here are a few ways to rebalance more tax-efficiently:

- Use new cash first. The easiest way to rebalance without selling is to put your new contributions toward the parts of your portfolio that are underweight.

- Rebalance in tax-advantaged accounts. Whenever you can, do your rebalancing inside an IRA or 401(k). Trades in these accounts don't trigger taxes, making them the perfect place to buy and sell.

- Look into tax-loss harvesting. If you do need to sell in a taxable account, you can sometimes offset your gains by selling other investments that are sitting at a loss.

Ready to use market sentiment to guide your rebalancing decisions? The Fear Greed Tracker provides real-time data on over 50,000 assets, helping you execute your strategy with greater confidence. Get started for free at FearGreedTracker.com.